Stephen Roach had a nice article today called The Handover Fallacy.

Point by point Roach dismisses the idea that there is going to be a smooth transition from US consumer spending to spending elsewhere that will drive the world economy forward. I do not buy that idea and neither does Roach. Let's tune in.

Fallacy #1 - The Capex Handover

Roach:

The capex handover is at the top of everyone’s list these days. That’s especially the case with respect to the US economy. There is a presumption that consumer fatigue is about to give way to support from the business sector. Awash in record cash flow and profitability, the wherewithal of Corporate America to spend on new plant, software, and equipment has never been greater. And so, there is hope that the baton of economic leadership is likely to be passed from consumption to capex -- a seamless transition that could well lead to another upside surprise for US economic growth.

The anemic pace of consumer demand in the final period of 2005 was even weaker than that recorded in the aftermath of 9/11 and, in fact, was the second weakest quarter of consumption growth of the past decade. If this is, in fact, the beginning of the end for the wealth-dependent American consumer -- hardly idle conjecture as the housing sector now starts to roll over -- hopes for a capex handover may be dashed.

Mish:

Given that consumer spending is 70% of GDP, exactly why should businesses be expanding production if consumer spending slows? It idea is as silly as it is pervasive. Instead we are likely to see share buybacks, IPOs, mergers and acquisitions, leveraged buyouts, and spinoffs in a foolish attempt to drive prices higher. This is similar to what happened in Spring of 2000 and it is happening again. Stock buybacks and acquisitions at these prices, while staring at an inverted yield curve and likely recession is silly. Yet history is repeating.

Fallacy #2 - China, Japan, and Europe demand will replace US demand.

Roach:

Don’t count on it -- the arithmetic of this particular handover is daunting. US consumption totaled $8.7 trillion in 2005 -- about 25% greater than European consumption (at market exchange rates), 3.3 times the level of Japanese consumer demand, 8-9 times the size of Chinese consumption (depending on data revisions), and fully 20 times the size of overall consumer spending in India. That means it would be a tall order for any one of these economies to compensate for a shortfall in US consumer demand. The bottom line is that an imminent slowing of the American consumer probably spells a weakening of global consumption and world GDP growth.

Mish: It is nearly impossible to tell anyone aware of "The China Story" that China's demand is all that matters. Yet much of that demand from China is to produce goods for the US. There is no doubt that China is the growth story, but there is also no doubt that China is not yet fully prepared for a smooth baton handoff. Based on negative savings rates and a likely sustained drop in home prices, US consumer spending fueled by cash out refis and home equity lines of credit is about to fall dramatically. There is no way China can pick up the slack. Furthermore the UK consumer seems to be in the same boat as the US consumer. That makes the downside risk all the more precarious. On the basis of demographics, Europe and Japan are simply not going to pick up the slack either. Long term China remains the story, short term don't be so sure.

Fallacy #3 - A handover from an asset to an income driven US economy will save the day

Roach:

It’s a neat theory, but it won’t work as long as America’s private sector labor income generation remains decidedly subpar. In my view it would take a reversal of the global labor arbitrage -- and a related unwinding of many of the powerful forces of globalization that are driving it -- to kick-start America’s internal income-generating capacity. Barring an unlikely outbreak of protectionism, the odds of a shift away from globalization are low. That suggests that the pressures on US labor income growth are likely to remain intense for years to come.

Mish:

I have been asked time and time again: "What will it take for you to change your deflationary outlook?" My answer has not once changed changed: "Rising US wages and significant US job expansion". I see little likelihood of this happening anytime soon. Furthermore, unlike Roach, I disagree that protectionism will do anything but make matters worse. Surely Roach is aware of the problems caused by the Smoot Hawley Tariffs in the 1930's. Protectionism is bound to throw more people out of work than any supposed benefit from increased wages.

Fallacy #4 - There will be a smooth transition from the Greenspan Fed to a Bernanke FED

Roach:

The Maestro turns over his baton to Ben Bernanke this week. Many argue that forward-looking financial markets have already discounted any risks associated with this historic event. With unusually tight credit spreads and low equity volatility pointing to an absence of risk in the price of risky assets, I find that assessment hard to buy. But I also think it misses the basic point of what this changing of the guard at the world’s most important central bank is all about. When he leaves his office on 31 January, Alan Greenspan will take his books, his papers, and his pictures off the wall. But the most important thing he will take with him will be the nearly 18 1/2 years of confidence that he has earned in the financial markets. Ben Bernanke walks in the next day as a very smart and talented man -- but with a clean slate on the confidence front. As I have noted previously, financial markets have an uncanny knack of quickly testing a new Fed chairman (See my 7 October 2005 dispatch, "Transition Curse"). This is not a handover to take lightly either.

Mish:

The problems facing Bernanke are simply impossible to resolve. Greenspan is leaving Bernanke with a housing bubble, a junk bond bubble, an enormous baby boomer time bomb, a Congress intent on cutting taxes and overspending, staggering budget deficits, staggering balance of trade issues, and growing threats of protectionism. Bernanke's writings prove he does not have a clue about the real cause of the great depression even though he is facing the greatest global economic set of problems since 1928. Bernanke has to face a Congress and president unlikely to bow to his every thought like they did Greenspan. Finally and most importantly, Bernanke unlike Greenspan does not have an internet boom or a housing boom to bail out his mistakes.

There is no "handover" to be had.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Monday 30 January 2006

Saturday 28 January 2006

Pro Forma GDP and the Feel Good Society

The LA Times is reporting GDP Data Are Weak and, Many Say, Off Base.

Why is it economists were cheerleading the 3rd quarter results and made no mention that sales were pulled forward, yet that excuse is made today? It seems to me that if big ticket numbers are bad, economists like Zandi want to discount them, otherwise they want to lead the parade. Why not just smooth the results like CSCO and GE did for so many years?

Then again, perhaps it's time to launch a new product that will keep everyone happy: pro forma GDP announcements. Who wants to hear bad news anyway? Wait a second. Attentive Mish bloggers realize we already have pro forma GDP reporting as noted in Grossly Distorted Procedures.

With that in mind, it seems we need to take pro forma GDP reporting to the next logical level by excluding "one time events" such as the 4th quarter disaster in auto sales. Still, that might not be enough to appease those wearing rose coloured glasses like Zandi or the super cheerleaders like Treasury Secretary John Snow.

"I would not read too much into today's numbers, Snow said. They are somewhat anomalous, reflecting some special factors. They are not consistent with other data on the U.S. economy which paint a picture of good growth."

Obviously then, we need to measure how things "feel" and incorporate those feelings back into the numbers. Unfortunately it seems "59% of respondents disapproved of the way President Bush was handling the economy". Wow, are those people right or are Snow and Zandi right?

It must be a sampling error. To ensure more accurate readings, the sampling algorithm needs to overweight input from those people whose opinions really matter such as the "feel good society", the Bush administration, and economists like Zandi. If we can just do that, we can come up with some truly astonishing pro forma GDP numbers bound to please everyone.

But why stop there? Why not futures on GDP numbers, options on those futures, and a full array of whisper numbers and other valuable products to further pad the pockets of the "feel good society"? That should make everyone feel better. Shouldn't it?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

The U.S. economy grew at a surprisingly weak 1.1% annual rate in the last three months of 2005, the Commerce Department said Friday, but many analysts said the economy was more robust than reported and would rebound in the current quarter. It was the slowest growth rate since the 0.2% posted in the fourth quarter of 2002, when the economy was struggling to recover from the 2001 recession.It feels like 4%! To who besides Zandi? Then again, if we want to measure the ultimate "feel good society" (CEOs and wall street brokers with their stock options, bonuses, and enormous base salaries) the GDP probably feels more like 68% than 1%. To the working class with falling real wages it might feel more like -5%.

The report came at a time when polls show that many Americans are skeptical about the economy's strength. A nationwide Los Angeles Times/Bloomberg poll, released Thursday, said 59% of respondents disapproved of the way President Bush was handling the economy.

The Bush administration and many experts, however, expressed doubt at the accuracy of the latest growth report, suggesting that it was at odds with other economic data. They predicted that the numbers would be revised upward.

"The fourth quarter was soft, but it wasn't this soft," said Mark Zandi, chief economist for Moody's Economy.com in West Chester, Pa. With recent reports suggesting strengthening job creation and business spending, "the economy is not growing at 1%. It feels more like 4%," Zandi said.

Business investment grew at 2.8%, down from a 8.5% gain in the third quarter. Federal government spending fell 7%, hit by a 13.1% drop in defense outlays. Exports grew 2.4%, and imports jumped 9.1%.

Consumer spending, which accounts for more than two-thirds of the economy, rose only 1.1%. That was far slower than the 4.1% gain in the third quarter and the slowest since the second quarter of 2001, when the economy was mired in recession. Purchases of big-ticket "durable" goods, such as cars, plunged 17.5%, the biggest fall in nearly 20 years.

Business investment grew at 2.8%, down from a 8.5% gain in the third quarter. Federal government spending fell 7%, hit by a 13.1% drop in defense outlays. Exports grew 2.4%, and imports jumped 9.1%.

But analysts said the numbers failed to tell the entire story.

Auto sales plunged because carmakers' "employee discount" offers during the summer pulled sales from the fourth quarter into the third. Excluding big-ticket goods such as autos, consumer spending actually grew faster in the fourth quarter than in the previous period.

Businesses also appeared to have pushed spending on vehicles into the summer, economist Zandi said. And the fall in defense spending didn't seem logical given the continuing Iraq war. Some outlays may have been pushed back or forward, he said.

Government spending on hurricane recovery efforts "didn't show up at all" in the report, Zandi said, suggesting that data collectors had incomplete figures on government relief checks for victims of hurricanes Katrina and Rita. "When lots of [unusual] things are going on, it's easier to get it wrong."

Why is it economists were cheerleading the 3rd quarter results and made no mention that sales were pulled forward, yet that excuse is made today? It seems to me that if big ticket numbers are bad, economists like Zandi want to discount them, otherwise they want to lead the parade. Why not just smooth the results like CSCO and GE did for so many years?

Then again, perhaps it's time to launch a new product that will keep everyone happy: pro forma GDP announcements. Who wants to hear bad news anyway? Wait a second. Attentive Mish bloggers realize we already have pro forma GDP reporting as noted in Grossly Distorted Procedures.

With that in mind, it seems we need to take pro forma GDP reporting to the next logical level by excluding "one time events" such as the 4th quarter disaster in auto sales. Still, that might not be enough to appease those wearing rose coloured glasses like Zandi or the super cheerleaders like Treasury Secretary John Snow.

"I would not read too much into today's numbers, Snow said. They are somewhat anomalous, reflecting some special factors. They are not consistent with other data on the U.S. economy which paint a picture of good growth."

Obviously then, we need to measure how things "feel" and incorporate those feelings back into the numbers. Unfortunately it seems "59% of respondents disapproved of the way President Bush was handling the economy". Wow, are those people right or are Snow and Zandi right?

It must be a sampling error. To ensure more accurate readings, the sampling algorithm needs to overweight input from those people whose opinions really matter such as the "feel good society", the Bush administration, and economists like Zandi. If we can just do that, we can come up with some truly astonishing pro forma GDP numbers bound to please everyone.

But why stop there? Why not futures on GDP numbers, options on those futures, and a full array of whisper numbers and other valuable products to further pad the pockets of the "feel good society"? That should make everyone feel better. Shouldn't it?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Friday 27 January 2006

Spinoffs, Merger Mania, and a GDP Warning Shot

Let's consider the GDP numbers for the 4th quarter of 2005:

Growth in the U.S. economy slowed dramatically to a 1.1% annual rate in the fourth quarter, the weakest growth in three years, the Commerce Department estimated Friday. The slowdown in real gross domestic product from 4.1% in the third quarter to 1.1% in the fourth was largely due to weak auto sales, slower business investment, a rise in imports and a large drop in federal spending. Inventory building was the main engine of growth in the quarter. Final sales fell 0.3%, the first decline since 2001. The core personal consumption expenditure price index rose at a 2.2% annual rate in the quarter. For all of 2005, the economy grew 3.5%, down from 4.2% in 2004. The personal savings rate was negative for the first year since 1933.

CNN Money notes GDP posts smallest gain in 3 years.

Does any of this remind anyone of March 2000? Here we are with housing obviously peaked, a FED merrily hiking away with 14 consecutive hikes, a GDP bordering on recession, a yield curve that is inverted, yet there is a stock market buy the dip mentality feeding frenzy unlike any we have seen since 2000. Speculation is rampant. Companies are going to the junk bond market to raise funds just to buyback shares. They all seem to want to burn up whatever cash hoard they have now.

Roll the dice baby. Is Chipotle worth 80 times earnings? Of course not. Who cares, anyway? All that matters is that it is going up. By the way, does anyone remember the flame out with Krispy Kreme Dougnnuts (KKD)? Pull up a chart and take a look.

In Has the FED already overshot? I made the case that the FED has indeed already overshot. I am sticking to my guns here. The FED has already overshot. I think the turndown in housing and GDP proves it.

Furthermore, unless the FED is stupid they know it. The problem is they created not only a housing bubble but they are also to blame for the repeat of the spinoff, merger mania, and leveraged buyout madness of 2000. If the FED can not rein in this madness not only will it be dealing with the housing bubble it created, but it will also have to deal with companies wrecking their balance sheets a second time.

Welcome to the FED Ben Bernanke. I am sure the upcoming recession welcomes you as well. It seems to me you are damned if you do and damned if you don't. So which is it?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

- Today the BEA published the GDP "advance release" .

- Next month we will see the "preliminary figures".

- After that we will see the "revised preliminary figures".

- The "final numbers" will be published when no one is looking.

- The "revised final numbers" will come out when someone wants to backdate the start of the upcoming recession.

Growth in the U.S. economy slowed dramatically to a 1.1% annual rate in the fourth quarter, the weakest growth in three years, the Commerce Department estimated Friday. The slowdown in real gross domestic product from 4.1% in the third quarter to 1.1% in the fourth was largely due to weak auto sales, slower business investment, a rise in imports and a large drop in federal spending. Inventory building was the main engine of growth in the quarter. Final sales fell 0.3%, the first decline since 2001. The core personal consumption expenditure price index rose at a 2.2% annual rate in the quarter. For all of 2005, the economy grew 3.5%, down from 4.2% in 2004. The personal savings rate was negative for the first year since 1933.

CNN Money notes GDP posts smallest gain in 3 years.

The nation's economy grew at its slowest pace in three years in the fourth quarter, according to the government's gross domestic product report Friday, which came in far weaker than economists' forecasts.Well, the bad news buyers were out in force again today on the mistaken notion that lower interest rates will save this economy. I have news for them: It won't. Furthermore, the more merger mania, buybacks, leveraged buyouts, and other nonsense like yesterday's Chipotle IPO Fiesta just might keep the FED hiking far longer than they might otherwise be inclined to do. Let's take a look at the latest fiesta:

The broad measure of the nation's economic activity showed an annual growth rate of 1.1 percent in the fourth quarter, down from the 4.1 percent growth rate in the final reading of third-quarter growth. Economists surveyed by Briefing.com had forecast a 2.8 percent growth rate in the fourth quarter.

Treasury Secretary John Snow tried to downplay the disappointing report on the nation's economic strength.

"The preliminary estimate of fourth quarter 2005 GDP is inconsistent with the underlying strength of the U.S. economy," he said in a statement. "I would not read too much into today's numbers. They are somewhat anomalous, reflecting some special factors. They are not consistent with other data on the U.S. economy which paint a picture of good growth."

[Mish Question: Exactly what data are you looking at Mr. Snow? Don’t you think it’s high time you toss that “paint by numbers” picture are you working on and look at the real world? That’s the problem with these “paint by numbers” kits. There never seems to be a storm cloud on the horizon.]

"The sharp pullback in economic growth during the final three months of 2005 shows the law of gravity has not been repealed," said Bernard Baumohl, executive director of the Economic Outlook Group. "When consumers are burdened with heavy debt loads, rising interest rates, higher energy costs, no personal savings and household income growth that falls below inflation, something had to give. This retrenchment in spending was generally foreseen, though economists weren't sure on the timing and magnitude."

Anthony Chan, chief economist for JPMorgan Private Client Services, said that any concern among investors about slower growth was more than balanced by their glee that the report could stop the Federal Reserve from raising interest rates after its Jan. 31 meeting, at which another quarter-percentage point hike is widely expected.

"The collapse of growth will serve as an incentive to stop the Fed from overshooting (on rate hikes)," said Chan.

[Mish Note: I guess we will see. We will explore this idea in just a bit]

David Wyss, chief economist for Standard & Poor's, said the GDP report changed his mind about what the Fed would do on rates.

"At this point I think the Fed pauses after the next rate hike," he said. "I had been looking for one more hike, although I had thought the chances were just a little better than 50-50. Now I think it's a little less than 50-50. Of course we'll get a lot more numbers before that Fed meeting (March 28)."

A big part of the slowdown was a 17 percent drop in spending on durable goods in the quarter, particular on cars and aircraft, as well as an unexpected 13 percent drop in government spending on national defense.

A nearly month-long strike at Boeing in September affected aircraft deliveries in the third quarter. And auto purchases, which saw sales record in the summer due to "employee pricing" offers from the Big Three automakers, fell 8 percent compared to a year earlier and 18 percent compared to the third quarter of 2005 due to the lack of remaining 2005 models that normally would have been purchased in the fall.

The drop in spending on motor vehicles was responsible for a 2.06 percentage point drop in the GDP by itself. The drop in military spending accounted for another 0.66 percentage point decline in the fourth quarter GDP, after adding 0.46 percentage point to the third quarter GDP growth.

"We knew the car sector was weak. Almost the entire surprise was the drop in government defense spending," said Wyss, commenting on the surprise. "Maybe the war is over but more likely you often get these oddities at the beginning of the fiscal year (that starts Oct. 1) because Department of Defense plays cash management games."

"I am confident the Pentagon will be spending more money at some time in 2006," Wyss said. "

[Mish note: I am confident of that as well. $300 billion wasted in Iraq is not enough to satisfy this administration.]

Part of the problem, a lot of the quarterly data has been distorted by (Hurricane) Katrina. We need another quarter to figure out what's going on. I think it's clear things are slowing down, the question is how much they're slowing down."

[Mish note: Katrina was indeed a distortion. All the "broken window theory" proponents are now seeing the payback. Any strength shown on account of hurricane cleanup was a mirage. Think back. How many times did the press talk about all the jobs it would create to rebuild New Orleans. It's sad economics, and obviously wrong, when CNBC cheerleaders proclaim disaster are good for the economy, yet they do it every time. I heard some say that it would be good for homebuilders.]

The most immediate impact could be making it more difficult for President Bush's speech writers to point to the strength of the economy in his State of the Union address Tuesday night. The president said Thursday that economic strength would be one of the subjects he will raise when campaigning for Republicans in this year's Congressional elections.

"They don't have a lot of tail wind with this number," [Chan] said.

[Mish note: Not only is there not a tail wind, that is a full force gale blowing in this economy's face. I believe the GDP actually went negative in the 4th quarter. For a better understanding why please read Grossly Distorted Procedures. If you are not aware of the lies and silliness behind the GDP numbers, that article might prove to be a real eye opener.]

Investors piled into the initial public offering of Chipotle Mexican Grill Thursday. But as the stock gets a chance to simmer in the market, investors could find that their optimism about the burrito chain is based on a hill of beans. After the 7.9-million-share offering priced at $22 a share, Chipotle shares doubled to close at $44 Thursday, after reaching as high as $48.28. Chipotle sold 6.1 million shares in the deal, raising about $134 million, while its parent, McDonald's sold 1.8 million shares. Morgan Stanley and S.G. Cowen led the underwriters. The casual dining chain's dizzying debut marked the biggest opening-day gain for a U.S. IPO since late 2000, according to Thomson Financial. At $44, shares of Chipotle are trading at roughly 80 times earnings. Meanwhile, Applebee's and Ruby Tuesday are trading closer to 20 times earnings, making Chipotle's valuation look laced with some irrational exuberance, even when its growth prospects are accounted for.The article claims that McDonalds is acting on "shareholder pressure" to boost the stock price. McDonalds is going the spinoff route to "unleash shareholder value". Other companies are doing the reverse. For them it is "merger mania" in an attempt to boost stock prices. One such deal resulted in a huge bidding war between Proctor & Gamble and Boston Scientific over Guidant. I note today that regulatory action could kill Guidant deal.

After the offering, McDonald's will have an 88% voting interest in Chipotle and a 69% economic interest. The fast food giant's decision to sell part of Chipotle in the public market was announced last fall, amid shareholder pressure to take action to boost its stock price.

Does any of this remind anyone of March 2000? Here we are with housing obviously peaked, a FED merrily hiking away with 14 consecutive hikes, a GDP bordering on recession, a yield curve that is inverted, yet there is a stock market buy the dip mentality feeding frenzy unlike any we have seen since 2000. Speculation is rampant. Companies are going to the junk bond market to raise funds just to buyback shares. They all seem to want to burn up whatever cash hoard they have now.

Roll the dice baby. Is Chipotle worth 80 times earnings? Of course not. Who cares, anyway? All that matters is that it is going up. By the way, does anyone remember the flame out with Krispy Kreme Dougnnuts (KKD)? Pull up a chart and take a look.

In Has the FED already overshot? I made the case that the FED has indeed already overshot. I am sticking to my guns here. The FED has already overshot. I think the turndown in housing and GDP proves it.

Furthermore, unless the FED is stupid they know it. The problem is they created not only a housing bubble but they are also to blame for the repeat of the spinoff, merger mania, and leveraged buyout madness of 2000. If the FED can not rein in this madness not only will it be dealing with the housing bubble it created, but it will also have to deal with companies wrecking their balance sheets a second time.

Welcome to the FED Ben Bernanke. I am sure the upcoming recession welcomes you as well. It seems to me you are damned if you do and damned if you don't. So which is it?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Thursday 26 January 2006

Another Week - Another 12 hour sale at Centex

Centex Homes - Washington DC - 12 Hour Sale!

Obviously there was never a better time to buy. Right?

Then again weren't they saying ....

There was never a better time to buy some $100,000 ago?

Some propose that the FED will lower rates soon and stop this decline.

Unfortunately

http://globaleconomicanalysis.blogspot.com/

- $100,000 off

- 100% financing

- Seller pays all closing costs

- 9 locations in Virginia, West Virginia, Maryland, Delaware

Obviously there was never a better time to buy. Right?

Then again weren't they saying ....

There was never a better time to buy some $100,000 ago?

Some propose that the FED will lower rates soon and stop this decline.

Unfortunately

- You can't do a refi when you are underwater on your house.

- You can't do a refi if credit standards rise.

- You can't do a refi at a lower rate if your credit sucks.

- You can't do a refi if you are out of a job.

- When psychology changes there will not be many buyers either.

http://globaleconomicanalysis.blogspot.com/

Wednesday 25 January 2006

Greenspan's Conundrum and UK Gilt Yields

SkyNews is writing UK Manufacturing Jobs Go.

Input prices are soaring, yet output prices are not (expect where prices are inelastic).

Housing prices soared because of nonsensical credit standards, and that credit seems to be drying up.

Those are the facts.

Those will be the facts regardless of what the US$ or the British Pound does.

That is why those focusing on the supposedly inflationary effects of a falling pound or a falling US$ are wrong. That is also why the FED and the ECB are wrong to be worried about rising energy prices. There will be no passthru unless and until there is an overall increase in the ability for consumers to pay higher prices. I see little evidence of rising wages in either the UK or the US. Instead I see 14 consecutive rate hikes in the US that are now hurting both home prices and credit lending.

Economic Factors

Mish note to inflationists:

If these conditions persist, there simply is no way to get inflation out of this mess.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Around 25,000 jobs were lost in the manufacturing industry over the past three months, says the CBI's latest survey.Hmmm. Let's see.

Manufacturers have been struggling to pass on rising costs to customers as customers themselves tighten their economic belts.

Firms hampered by sharp rises in the cost of gas and oil cut staff numbers in a bid to relieve squeezed profit margins, employers' body the CBI said.

The total number of jobs lost in the manufacturing sector over the past year was 106,000, the CBI's quarterly industrial trends study revealed.

"Conditions for manufacturers are getting increasingly tough as costs continue their seemingly inexorable rise," said the CBI's Ian McCafferty.

"But weak demand keeps prices down, squeezing already thin profitmargins even further.

"The sustained high level of oil and sharply increased gas prices have driven up energy and raw material costs.

"Manufacturers are continuing to respond by cutting employment to curb the wage bill and boosting investment in efficiency-improving measures."

- Oil prices rise.

- Natural gas prices rise.

- Raw materials prices rise.

- Weak demand prevents passing along those prices.

- Manufacturers respond by cutting employment.

- If employment is cut, what will that do to demand?

- If demand falls, what will that do to prices?

- What happens when Brown is forced to raise taxes?

- When did the slowdown start?

- If input costs do not matter in the UK will they matter in the US?

- What happens to demand if Bush raises taxes or cuts government spending?

- If costs can not be passed on will it matter if the US$ falls?

- What happens if housing slumps?

- Whether or not we are talking US or UK, prices either can or can not be passed on.

- Right now it seems that they can't, at least in the UK.

- Demand for goods is falling.

- UK unemployment is rising because of falling demand.

- If Brown raises taxes it will further decrease demand for goods and further increase unemployment.

- Prices at the pump and heating costs can and have been passed on because gasoline and heating oil prices are inelastic.

- Medical expenses are also inelastic. If you need an operation to save your life you will get it regardless of what it costs.

- Laying off workers will decrease the ability of consumers to pay higher prices.

- Problems started happening in the UK with a slump in housing.

- Problems are now starting in the US over housing on a 6-8 month time lag vs the UK.

- If credit dries up people simply can not buy what they can not afford.

- Credit is starting to dry up in the US when looking at home equity lines and cash out refis.

- A falling US$ is mostly irrelevant to the equation. Prices simply can not rise unless beyond people's ability to pay unless further credit is extended.

Input prices are soaring, yet output prices are not (expect where prices are inelastic).

Housing prices soared because of nonsensical credit standards, and that credit seems to be drying up.

Those are the facts.

Those will be the facts regardless of what the US$ or the British Pound does.

That is why those focusing on the supposedly inflationary effects of a falling pound or a falling US$ are wrong. That is also why the FED and the ECB are wrong to be worried about rising energy prices. There will be no passthru unless and until there is an overall increase in the ability for consumers to pay higher prices. I see little evidence of rising wages in either the UK or the US. Instead I see 14 consecutive rate hikes in the US that are now hurting both home prices and credit lending.

Economic Factors

- Global wage arbitrage is hugely understated as a deflationary force.

- Rising energy costs are hugely overstated as an inflationary force.

Mish note to inflationists:

If these conditions persist, there simply is no way to get inflation out of this mess.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Tuesday 24 January 2006

Is the US current account balance sustainable?

According to a study by Fed economist John Rogers and Professor Charles Engel , the U.S. current account deficit may be near optimal levels based on expected economic growth trends among wealthy countries. Let's take a look:

Gee that's nice.

We think we are right but if not, we are on the path to ruin.

Once again we see economists projecting forever into the future the trend they see today. Since 1993 the US GDP has been underestimated so now the assumptions have been revised to "expect a large increase in U.S. share of GDP".

One look at China and India should be enough to convince anyone that now is precisely the wrong to be increasing assumptions about the US. The economists missed the dot com boom, the housing boom, the internet revolution, and now with China, India, and other countries coming of age the US is supposed to be the engine of growth for the world? Marc Faber warns of projecting trends forever into the future in his classic book "Tomorrow's Gold". I highly recommend it.

If ignoring China and India was not bad enough, Rogers and Engel seem to ignore how grossly overstated our GDP is with hedonics and imputations. Please see Grossly Distorted Procedures for an explanation.

The two biggest distortions are the amount of rent you pay yourself if you own a house, and the value of the free checking account that you should be paying your bank for. The Government imputes the total value of "free checking accounts" to be worth a mere $335.2 billion and adds that number to the GDP. The government also assumes that homeowners are paying themselves $153.8 billion in rent. That too is added to the GDP. The Total Of All Distortions (TOAD) is $3892 billion out of a total GDP of $11004 billion. My math says the US GDP is 35% overstated. Bear in mind that is what the government readily admits to. Could it be that the real TOAD is far uglier? By the way those are 2003 numbers, the government is way behind on reporting imputations. It is likely the distortions have grown more extreme. The bottom line is simple: lop off one to two points off the GDP for a more better estimate as to what is really happening. That just might help explain why the jobs growth during this recovery has been so anemic.

Just as Rogers and Engel are promoting the "Free Lunch Theory", Timothy Geithner, the New York Federal Reserve president proclaims the account deficit 'unsustainable'.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Dramatic growth in the U.S. share of gross domestic product - net of investment and government spending - among wealthy countries has been "one of the most striking economic developments of the last 25 years," according to the study by Fed economist John Rogers and University of Wisconsin Professor Charles Engel.Of course they readily admit: If simplifications and assumptions in the study are wrong, "it may turn out, as many have been warning, that the deficits have put the U.S. on the path to ruin".

While noting major caveats, the study finds "the size of the U.S. current account deficit may be justifiable if markets expect further growth in the U.S. share of advanced-country GDP." A country's current and expected-future share of world economic output determines its optimal ratio of consumption to output, Engel and Rogers say.

The authors say their modeling could contain important flaws undermining the idea that the U.S. current account reflects optimal consumer decisions. If simplifications and assumptions in the study are wrong, "it may turn out, as many have been warning, that the deficits have put the U.S. on the path to ruin," the economists say.

The study's findings could falter if East Asian economies reverse their role as large net savers and lenders in international capital markets, or if the U.S. loses the "exorbitant privilege" that allows it to earn higher rates on its foreign investments than foreigners earn on investments in the U.S., they say.

The economists also say they were unable to reach firm conclusions about the path of foreign exchange rates over the next 25 years.

But their study cites long-term economic growth trends that appear to justify the size of the U.S. current account deficit relative to economic growth expectations.

Since 1993 consensus long-term forecasts have consistently and widely underestimated U.S. economic growth relative to G7 countries as a whole, the study says. "The current forecasts for the future, however, show that the markets expect a large increase in U.S. share of GDP - almost precisely the amount that we calculate would make the current level of deficit optimal," it says.

Federal Reserve Chairman Alan Greenspan and other Fed officials have said recent sharp growth in the U.S. current account deficit - the broadest gauge of the country's trade gap with the rest of the world - can't persist indefinitely. The deficit reached $195.8 billion, or 6.2% of GDP, in the third quarter of 2005, and it is expected to have hit a record for 2005 as a whole.

In a speech last month, Greenspan suggested he has become less concerned about the trade deficit's potential to spark financial market turmoil because the deficit stems partly from a global increase in cross-border trade and investment. But he also warned of dangers from unchecked U.S. government budget deficits and the potential for protectionist barriers to international trade.

Gee that's nice.

We think we are right but if not, we are on the path to ruin.

Once again we see economists projecting forever into the future the trend they see today. Since 1993 the US GDP has been underestimated so now the assumptions have been revised to "expect a large increase in U.S. share of GDP".

One look at China and India should be enough to convince anyone that now is precisely the wrong to be increasing assumptions about the US. The economists missed the dot com boom, the housing boom, the internet revolution, and now with China, India, and other countries coming of age the US is supposed to be the engine of growth for the world? Marc Faber warns of projecting trends forever into the future in his classic book "Tomorrow's Gold". I highly recommend it.

If ignoring China and India was not bad enough, Rogers and Engel seem to ignore how grossly overstated our GDP is with hedonics and imputations. Please see Grossly Distorted Procedures for an explanation.

The two biggest distortions are the amount of rent you pay yourself if you own a house, and the value of the free checking account that you should be paying your bank for. The Government imputes the total value of "free checking accounts" to be worth a mere $335.2 billion and adds that number to the GDP. The government also assumes that homeowners are paying themselves $153.8 billion in rent. That too is added to the GDP. The Total Of All Distortions (TOAD) is $3892 billion out of a total GDP of $11004 billion. My math says the US GDP is 35% overstated. Bear in mind that is what the government readily admits to. Could it be that the real TOAD is far uglier? By the way those are 2003 numbers, the government is way behind on reporting imputations. It is likely the distortions have grown more extreme. The bottom line is simple: lop off one to two points off the GDP for a more better estimate as to what is really happening. That just might help explain why the jobs growth during this recovery has been so anemic.

Just as Rogers and Engel are promoting the "Free Lunch Theory", Timothy Geithner, the New York Federal Reserve president proclaims the account deficit 'unsustainable'.

Timothy Geithner, president of the New York Federal Reserve, on Monday dismissed the view that the US current account deficit was sustainable, suggesting the risk of a sudden fall in the dollar would grow the longer the trade gap widened.I suppose it is refreshing to see the FED saying something that makes some semblance of sense. The problem however, is that under Greenspan the FED let problem after problem get out of hand while he became the top cheerleader for the US productivity miracle. As for me, I think we are now so far down the path to ruin, that we can all but rule out the "gradual and benign" in favor of a "more precipitous and damaging" ending.

In a speech at the Royal Institute of International Affairs in London, Mr Geith-ner said the problem could not necessarily be expected to solve itself.

“Time does not necessarily help. The longer these gaps continue to build, the greater the ultimate adjustment required, and the greater the risks that accompany that process,” he said.

“The plausible outcomes range from the gradual and benign to the more precipitous and damaging,” he said. “The size and duration of these [global] imbalances, perhaps the most visible of which is the US current account deficit, present challenges – and risks – for the world economy.”

“A prolonged continuation of the exchange rate ar-rangements that have given rise to the large increase in foreign official investments in US financial assets is unlikely to be consistent with the domestic requirements of those economies and for this reason many are already in the process of change,” he said.

“Even if we could be confident that the world would be comfortable financing the US on these terms for some time, that fact alone does not mean that it is prudent for the US to continue borrowing on this scale.”

Mr Geithner repeated his call for US politicians to reduce the budget deficit. The fact that the US is using much of the money borrowed from abroad to finance public spending, he said, increased the dangers. If it was being invested in the productive capacity of the US tradeable goods industries, this would at least help the US to pay back its foreign obligations.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Sunday 22 January 2006

Iranian Oil Bourse Nonsense

I must have seen five different articles on the Iranian Oil Bourse over the past week or so. I have probably seen a hundred posts over the last year that the war in Iraq was because Hussein was going to price oil in Euros. These articles all make for sensational headlines but it is all nonsense. Perhaps we went to war in Iraq with intention of stealing their oil, but we sure did not go to war over pricing.

Following are some of the silliest statements I have ever heard on the subject:

Many have criticized Bush for staging the war in Iraq in order to seize Iraqi oil fields. However, those critics can’t explain why Bush would want to seize those fields—he could simply print dollars for nothing and use them to get all the oil in the world that he needs. He must have had some other reason to invade Iraq.

Benefits from Iraqi oil fields are hardly worth the long-term, multi-year military cost. Instead, Bush must have went into Iraq to defend his Empire. Indeed, this is the case: two months after the United States invaded Iraq, the Oil for Food Program was terminated, the Iraqi Euro accounts were switched back to dollars, and oil was sold once again only for U.S. dollars. No longer could the world buy oil from Iraq with Euro. Global dollar supremacy was once again restored. Bush descended victoriously from a fighter jet and declared the mission accomplished—he had successfully defended the U.S. dollar, and thus the American Empire.

This is what the author is saying

1) The oil fields are not worth holding

2) Bush could just print dollars and buy oil

3) What oil is priced in is more important than the oil itself.

Number 1 is laughable. The author cites the cost of the war as a detriment yet proposes Bush could just print dollars to buy oil but somehow can not print dollars to pay for a war. Of course the author ignores the consequences of printing dollars of number 2. The author also forgets that the US could just print dollars and buy Euros. Number 3 is of course patently absurd.

These articles are so obviously absurd I wonder why people keep shoving them at me.

Yet, here is another silly article that keeps making the rounds:

The Iranian Threat: The Bomb or the Euro?

Back in October I staked a claim on how silly these ideas were with

Oil Priced in Euros. Would it matter?

Perhaps a better case for how silly this all is was made in Strange ideas about the Iranian oil bourse.

The point I would like to make is that regardless of the pricing unit on oil there will likely be a gradual shift away from US dollar assets and US dollar currency reserves. That is the key issue, and it will NOT take oil to be priced in Euros for that to happen any more that it will take gold to be priced in Euros for China, Russia, Argentina, and other countries to start accumulating gold.

We simply did not go to war with Iraq because Iraq was about to price oil in Euros.

Can we stop the nonsense?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Following are some of the silliest statements I have ever heard on the subject:

Many have criticized Bush for staging the war in Iraq in order to seize Iraqi oil fields. However, those critics can’t explain why Bush would want to seize those fields—he could simply print dollars for nothing and use them to get all the oil in the world that he needs. He must have had some other reason to invade Iraq.

Benefits from Iraqi oil fields are hardly worth the long-term, multi-year military cost. Instead, Bush must have went into Iraq to defend his Empire. Indeed, this is the case: two months after the United States invaded Iraq, the Oil for Food Program was terminated, the Iraqi Euro accounts were switched back to dollars, and oil was sold once again only for U.S. dollars. No longer could the world buy oil from Iraq with Euro. Global dollar supremacy was once again restored. Bush descended victoriously from a fighter jet and declared the mission accomplished—he had successfully defended the U.S. dollar, and thus the American Empire.

This is what the author is saying

1) The oil fields are not worth holding

2) Bush could just print dollars and buy oil

3) What oil is priced in is more important than the oil itself.

Number 1 is laughable. The author cites the cost of the war as a detriment yet proposes Bush could just print dollars to buy oil but somehow can not print dollars to pay for a war. Of course the author ignores the consequences of printing dollars of number 2. The author also forgets that the US could just print dollars and buy Euros. Number 3 is of course patently absurd.

These articles are so obviously absurd I wonder why people keep shoving them at me.

Yet, here is another silly article that keeps making the rounds:

The Iranian Threat: The Bomb or the Euro?

Back in October I staked a claim on how silly these ideas were with

Oil Priced in Euros. Would it matter?

Perhaps a better case for how silly this all is was made in Strange ideas about the Iranian oil bourse.

For starters, you don't need to acquire any U.S. assets in order to purchase a barrel of oil that is priced in dollars. You could pay with eurodollars, which are dollar-denominated accounts that could be issued by any bank anywhere in the world.The KEY issue behind all of this hype is that of reserve status of the US dollar. The "Bourse Nonsense" seems to imply two things that simply are not true:

And even if the oil were purchased with dollars drawn on a U.S. bank, there is no reason at all that the seller needs to retain the proceeds in that form. Those selling oil could convert those dollars back to euros or Japanese yen or whatever their hearts desired, and likewise could convert euros obtained through sales on an Iranian bourse back into dollars, if they wished. What ultimately determines the demand for dollars is not the unit of account for the transaction, but rather the desired asset holdings of those who are accumulating the wealth.

You could buy gold right now in New York for dollars or in London for pounds. Which one is cheaper? Guess what-- you'll pay exactly the same price either place once you make the currency conversion at the current exchange rate. The same will surely hold for crude oil.

And the notion that the U.S. dollar is currently "backed by oil" is so nonsensical that it is difficult even to fathom what that phrase is intended to convey. When we say that under a gold standard, the dollar is backed by gold, I know exactly what that means-- it means you can surrender dollars at any time to obtain a fixed amount of gold promised by the government. But if you surrender dollars on any given day in January 2006, how much oil are you going to get back?

It varies literally by the minute, and the rate at which dollars get exchanged for oil has nothing to do with the promises made by any government and everything to do with market fluctuations in supply and demand.

Which is also my explanation for the prevalence of these theories on the internet-- there is a demand for a deeply conspiratorial interpretation of world events, and always someone willing to supply such.

- Oil will have to be priced in euros (or some other currency) for the US dollar to lose reserve status.

- As long as oil remains priced in US dollars the US will retain reserve status.

The point I would like to make is that regardless of the pricing unit on oil there will likely be a gradual shift away from US dollar assets and US dollar currency reserves. That is the key issue, and it will NOT take oil to be priced in Euros for that to happen any more that it will take gold to be priced in Euros for China, Russia, Argentina, and other countries to start accumulating gold.

We simply did not go to war with Iraq because Iraq was about to price oil in Euros.

Can we stop the nonsense?

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Big News at Cisco?

PC Pro is reporting Cisco, the US networking giant has big plans to enter the mainstream consumer electronics market.

It was not long ago that Cisco missing or beating the street was market breaking news. The market went up or down based on Cisco. How would the market have reacted to this news in February of 2000? Today Google news seems far more relevant. My how times have changed. Cisco sells a commodity and looks to sell more commodities where the competition is even more intense. Who cares?

Microsoft is another bloated company.

The market goes up. The market goes down. No one really wants to buy or sell either one of them yet all the mutual funds think you "have to have them".

They are still labeled "growth companies" although their growth is long gone and likely never returning.

So why does Cisco feel the need to compete in a crowded electronics market?

Hmmmm. Could it be there is little growth left in routers or is it simply there is little growth left in Cisco routers? Either way is there a difference?

I think not.

To preserve some sort of lie about growth, Cisco just might go on a buying spree of overpriced companies. They did it before, why not try it again?

No one seems to have learned anything from 2000. In its heyday, Cisco went on various buying sprees, none of which really did much for the bottom line but it did make revenues go up. Corporations in general seem to have cash to burn after a 3 year runup, but with a yield curve about ready to invert and a consumer led recession coming up to boot, companies once again want to capture market share and increase revenues regardless of price.

Will Sony, Samsung and Philips be shaking in their boots or laughing out loud?

It will be a big waste of money if Cisco follows through with their plan.

At a market cap of $113 billion and no debt, Cisco would be wise to declare a big dividend and admit (like Microsoft) that it is just another overbloated giant with nowhere to go. If it returned 100% of earnings to shareholders as dividends there might be a reason to hold it. If it instead goes into debt trying to compete outside its core competence in a very competitive electronics market, it is without a doubt in for some extremely rough times.

I am ready for an attitude switch.

Corporations should forget about growth at any cost and instead start returning earnings with increased dividends. Fat chance. That will likely happen at the end of the bear market when companies should be looking for ways to expand growth.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Cisco is considering the production of radios, phones and stereo systems, according to the Financial Times, which interviewed Charles Giancarlo, the company's chief development officer.Yawn.

While the Internet fridge has long been held as an example of a high-tech white elephant, Cisco apparently believes the demand for increasing Net connectivity for a range of devices presents a new opportunity for the venerable networking company.

'Consumer electronics companies have been able to compete on a stand-alone device but the dynamics of the market are changing,' he told the FT. 'The Internet and new networking requirements are enough of a disruptor for us to enter a new market'.

While best known for network routers and switches, the acquisition of Linksys in 2003 already positioned the company in the home networking market (see Linksys frees Skype from the PC). And Giancarlo believes Cisco's existing relationships with major online players such as Google and Yahoo! will give it a further edge.

Cisco has clearly had its eye on the living room for a while though, with a string of pertinent acquisition including Scientific Atlanta, a US maker of set-top television boxes, and KiSS Technology, a Danish maker of Net-connected DVD players.

Whether the likes of Sony, Samsung and Philips will be shaking in their high-tech, branded boots remains to be seen, after all the consumer electronics is already a very competitive market.

It was not long ago that Cisco missing or beating the street was market breaking news. The market went up or down based on Cisco. How would the market have reacted to this news in February of 2000? Today Google news seems far more relevant. My how times have changed. Cisco sells a commodity and looks to sell more commodities where the competition is even more intense. Who cares?

Microsoft is another bloated company.

The market goes up. The market goes down. No one really wants to buy or sell either one of them yet all the mutual funds think you "have to have them".

They are still labeled "growth companies" although their growth is long gone and likely never returning.

So why does Cisco feel the need to compete in a crowded electronics market?

Hmmmm. Could it be there is little growth left in routers or is it simply there is little growth left in Cisco routers? Either way is there a difference?

I think not.

To preserve some sort of lie about growth, Cisco just might go on a buying spree of overpriced companies. They did it before, why not try it again?

No one seems to have learned anything from 2000. In its heyday, Cisco went on various buying sprees, none of which really did much for the bottom line but it did make revenues go up. Corporations in general seem to have cash to burn after a 3 year runup, but with a yield curve about ready to invert and a consumer led recession coming up to boot, companies once again want to capture market share and increase revenues regardless of price.

Will Sony, Samsung and Philips be shaking in their boots or laughing out loud?

It will be a big waste of money if Cisco follows through with their plan.

At a market cap of $113 billion and no debt, Cisco would be wise to declare a big dividend and admit (like Microsoft) that it is just another overbloated giant with nowhere to go. If it returned 100% of earnings to shareholders as dividends there might be a reason to hold it. If it instead goes into debt trying to compete outside its core competence in a very competitive electronics market, it is without a doubt in for some extremely rough times.

I am ready for an attitude switch.

Corporations should forget about growth at any cost and instead start returning earnings with increased dividends. Fat chance. That will likely happen at the end of the bear market when companies should be looking for ways to expand growth.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Friday 20 January 2006

Poof - 25% Underwater Overnight

How would you like to wake up in a house that declined 25% in value overnight?

If you are a proud Centex owner at "Martins Crossing" in Florida, it just happened to you.

SAVE $105,000 - Centex Close Out - NOW $294,000 - NEW Single Family Home in Martins Crossing - 4 Bedroom, 2 Bathroom, 2 Car Garage - 1,695 sf.

BEST DEAL OF THE YEAR!

Let's see.

Poof.

$105,000 just went up in smoke.

That ENTIRE subdivision just took a $100,000+ hit.

Wait a second.

This can't happen, can it?

They are not making land in Florida anymore are they?

People want to move to Florida right?

Did it matter?

This exact scenario is going to play out in bubble area, after bubble area, after bubble area.

The party has just started.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

If you are a proud Centex owner at "Martins Crossing" in Florida, it just happened to you.

SAVE $105,000 - Centex Close Out - NOW $294,000 - NEW Single Family Home in Martins Crossing - 4 Bedroom, 2 Bathroom, 2 Car Garage - 1,695 sf.

BEST DEAL OF THE YEAR!

Let's see.

Save $105,000$105,000/$399,000 = 26.32%

Now $294,000

=============

PP $399,000

Poof.

$105,000 just went up in smoke.

That ENTIRE subdivision just took a $100,000+ hit.

Wait a second.

This can't happen, can it?

They are not making land in Florida anymore are they?

People want to move to Florida right?

Did it matter?

This exact scenario is going to play out in bubble area, after bubble area, after bubble area.

The party has just started.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Thursday 19 January 2006

312 Million for This?

Toll Brothers, Meritage Homes and Simon Property Group Joint Venture announce the purchase of a 5,485-acre land parcel in Phoenix's Northwest Valley for $312 Million.

It is the largest real estate transaction in Arizona history.

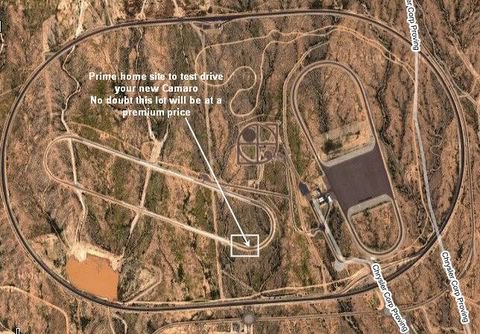

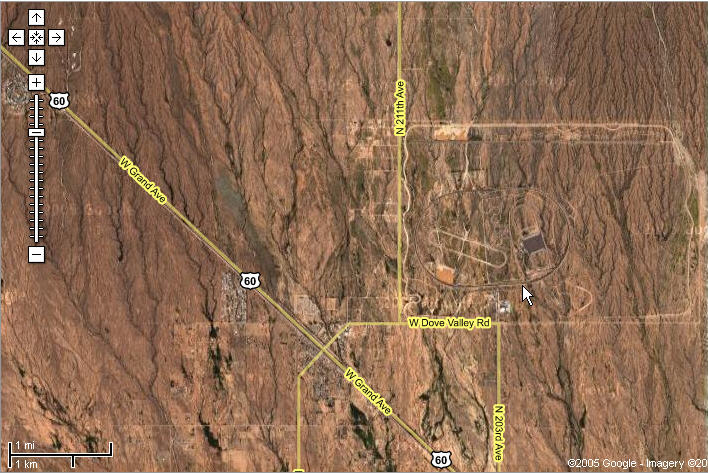

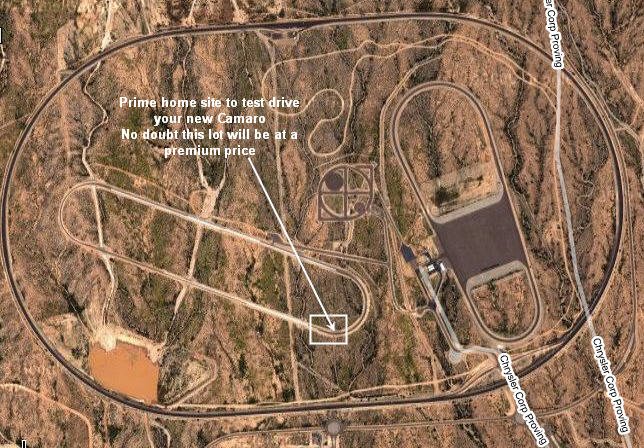

Enquiring Mish bloggers might be wondering exactly where "Phoenix's Magnificent Northwest Valley" is. Thru the wonder of Google satellite imagery I am pleased to show everyone the following pictures of just what that consortium of buyers got for their $312 million.

Here is this "highly coveted site".

It seems to be about 35 or 40 miles away from Phoenix.

The attraction? A commute from there to downtown during rush hour might be close to an hour each way and where will gas prices be in a couple of years anyway?

Let's zoom in looking for the attraction.

I do not see any do you?

Let's zoom in further.

There it is. I boxed it in. The premier spot to test drive your new Camaro, provided of course Toll Brothers decides to keep that test track up and running. If not, what the attraction?

Homebuilders Buried in Land

With that in mind, I note with interest this Street.Com article entitled Homebuilders Buried in Land. Enquiring Mish readers might want to know more so let's take a look at that too.

On that thought I just received another telepathic question. It's been a while since we have had one of those and here it is: "But Mish what about those fabulous PEs?"

Those PEs are a mirage. The homebuilders have negative cash flow and keep sinking every penny of their earnings into land, land, and more land at increasingly absurd prices as the article above addressed, and that transaction proved.

Here is the homebuilder picture:

Just two weeks ago I was told by a Real Estate Broker friend of mine that Atlanta was impervious to a slowdown and there would be no recession coming our way. I note with interest This ad by Centrex.

$60,000 off?

Everything is fine in Atlanta?

Everyone seems to think their area is impervious to a slowdown because of demographics, warm weather, an ocean, or whatever. That seems to be the key to this mania.

Well I have news for you.

An Interest Rate Squeeze does not care where you live. Prices matter as do prevailing rents. Home prices do not always go up. Please click on that link and see what I am talking about. I suspect Toll Brothers and Meritage Homes will find out in due time just how silly that purchase in Phoenix was. By then it will be too late. It is the overpayment for land that bankrupts homebuilders every cycle. This cycle will be no different.

Mish note: This article originally appeared in Whiskey and Gunpowder.

Following are three comments I received in response to that publication:

From: Connie

Subject: Phoenix real estate - I live here!!

I live in the east valley of Phoenix, and I can tell you things are really slowing down here, as existing homes are sitting unsold for weeks now and prices are dropping. I am planning to leave the area soon because there will not be any water here in the coming years and it will be a MAMMOTH problem. No one seems to care now but it is coming! I have been called numerous times to come to an opening of Dell Webb new project. I think they are having trouble getting interest in it and they keep saying they "haven't decided on prices yet" so what's up with that? Keep up the good work,

C.J. Phoenix, AZ

==================================================

Subject: $312 million for that?

Why buy land for housing development? They should've invested in a tract of mineral rich land in Nevada. At least when the housing market implodes they could start mining for gold, or sell it on to one of the big resource hungry blue chips. Or is there actually precious yellow metal under that ground they purchased near Phoenix that no-one is aware of?

Regards,

J.N.

==================================================

Subject: Phoenix Desert

Hi There,

You missed a major point. Where are they going to get the water for all those houses? The Colorado River is over subscribed. One of the worst droughts in history is going on there in Arizona right now. And those of us up here in the Rust Belt just cemented a deal so they cannot steal water from the Great Lakes. Oh well, in 20 years it will all be part of Mexico once again, anyway.

Keep up the great work!

S.B.

==================================================

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

It is the largest real estate transaction in Arizona history.

The Maricopa County property, which DaimlerChrysler currently utilizes as a vehicle endurance testing and development facility, is bound by 183rd Avenue on the east, 211th Avenue on the west, Dove Valley on the south and Joy Ranch Road on the north. DaimlerChrysler will continue to lease the property for the next few years, in order to plan and accommodate for the orderly transition of its testing operations.$312 million for 5,485 acres of desert with a testing track on it. That amounts to $56,882 dollars per acre of flat desert.

Toll Brothers and Meritage Homes each plan to build a significant number of homes on the site. Simon Property Group, Inc. has the option to purchase a substantial portion of the commercial property. Other parcels may be sold to third parties. Initial plans call for a mixed-use master planned community, which will include approximately 4,840 acres of single-family homes and attached homes. Approximately 645 acres of commercial and retail development will include schools, community amenities and open space. Initial homes sales are tentatively scheduled to begin in 2009. According to the approved General Plan, the site allows between 15,000 to 31,000 homes.

Robert I. Toll, chairman and chief executive officer of Toll Brothers, Inc., stated: "We are thrilled to have been chosen by DaimlerChrysler and to have teamed up with two excellent partners to develop this fabulous piece of real estate. The northwest area of Phoenix has experienced unprecedented popularity and this particular parcel is a highly coveted site."

Enquiring Mish bloggers might be wondering exactly where "Phoenix's Magnificent Northwest Valley" is. Thru the wonder of Google satellite imagery I am pleased to show everyone the following pictures of just what that consortium of buyers got for their $312 million.

Here is this "highly coveted site".

It seems to be about 35 or 40 miles away from Phoenix.

The attraction? A commute from there to downtown during rush hour might be close to an hour each way and where will gas prices be in a couple of years anyway?

Let's zoom in looking for the attraction.

I do not see any do you?

Let's zoom in further.

There it is. I boxed it in. The premier spot to test drive your new Camaro, provided of course Toll Brothers decides to keep that test track up and running. If not, what the attraction?

Homebuilders Buried in Land

With that in mind, I note with interest this Street.Com article entitled Homebuilders Buried in Land. Enquiring Mish readers might want to know more so let's take a look at that too.

Ed Wachenheim, a long-term value investor, agrees with the general view that homebuilder stocks are cheap right now. But the money manager, who was once a major owner of the sector, has sold off most of his positions because he's worried about the huge amount of land on builders' books.Another Telepathic Question

"My fear is that many of the companies took on too-large land positions at too-high prices. And that means that should the industry turn down that there is risk that there will be some impairment of land values," says Wachenheim, who runs Greenhaven Associates, a Purchase, N.Y.-based firm that manages $3.7 billion of capital, mostly for wealthy individuals.

It's difficult to determine if Wachenheim's concerns are justified and builders have been too aggressive in taking on new land. Builders report the dollar value of their total land holdings in quarterly filings, but nothing is usually said about the prices paid for individual parcels.

There also is no geographic breakdown to determine whether a builder like Pulte Homes has too much exposure to a frothy market like Las Vegas. All the public knows is that Pulte's total inventory of owned land was $5.3 billion for the quarter ending Sept. 30, up from $4.49 billion a year earlier. That amounts to 170,000 home lots, or roughly three years of supply, the company says.

But what if that's too much land to be holding in a slowing housing market?

The issue is of particular note since builders have spent the bulk of their earnings over the past few years buying land for future building. Although most builders have at least 50% of their lots controlled through options, a large amount of purchased land continues to be placed on balance sheets. As a result, the sector in general has seen negative cash flows for some time now.

"I have never seen a group, in 20 years of analysis, post negative cash flow from earnings for four of the last five years and prosper as a stock group without having to pay the piper," says Jim Poyner, an analyst for Palladian Research, an independent New York research house. Poyner thinks land impairments could begin popping up over the next year if builders start slashing prices on new homes for sale.

Robert Curran, a Fitch Ratings analyst who covers the builders, says it's premature to worry about land impairments now, but grants that the issue could arise in the future.

"There isn't anyone who really stands out as being overloaded on raw land on the balance sheet that is just sitting there," Curran says. It would take an economic recession or a really problematic regional housing market for there to be large land impairments, he adds. "If home prices come down, it doesn't mean you will write down land assets."

On that thought I just received another telepathic question. It's been a while since we have had one of those and here it is: "But Mish what about those fabulous PEs?"

Those PEs are a mirage. The homebuilders have negative cash flow and keep sinking every penny of their earnings into land, land, and more land at increasingly absurd prices as the article above addressed, and that transaction proved.

Here is the homebuilder picture:

- Homebuilders have negative cash flows

- Homebuilders put the bulk of their profits into buying more land at absurd prices

- Homebuilders are totally ignoring the yield curve

- Homebuilders are discounting the odds of a recession

Just two weeks ago I was told by a Real Estate Broker friend of mine that Atlanta was impervious to a slowdown and there would be no recession coming our way. I note with interest This ad by Centrex.

$60,000 off?

Everything is fine in Atlanta?

Everyone seems to think their area is impervious to a slowdown because of demographics, warm weather, an ocean, or whatever. That seems to be the key to this mania.

Well I have news for you.

An Interest Rate Squeeze does not care where you live. Prices matter as do prevailing rents. Home prices do not always go up. Please click on that link and see what I am talking about. I suspect Toll Brothers and Meritage Homes will find out in due time just how silly that purchase in Phoenix was. By then it will be too late. It is the overpayment for land that bankrupts homebuilders every cycle. This cycle will be no different.

Mish note: This article originally appeared in Whiskey and Gunpowder.

Following are three comments I received in response to that publication:

From: Connie

Subject: Phoenix real estate - I live here!!

I live in the east valley of Phoenix, and I can tell you things are really slowing down here, as existing homes are sitting unsold for weeks now and prices are dropping. I am planning to leave the area soon because there will not be any water here in the coming years and it will be a MAMMOTH problem. No one seems to care now but it is coming! I have been called numerous times to come to an opening of Dell Webb new project. I think they are having trouble getting interest in it and they keep saying they "haven't decided on prices yet" so what's up with that? Keep up the good work,

C.J. Phoenix, AZ

==================================================

Subject: $312 million for that?

Why buy land for housing development? They should've invested in a tract of mineral rich land in Nevada. At least when the housing market implodes they could start mining for gold, or sell it on to one of the big resource hungry blue chips. Or is there actually precious yellow metal under that ground they purchased near Phoenix that no-one is aware of?

Regards,

J.N.

==================================================

Subject: Phoenix Desert

Hi There,

You missed a major point. Where are they going to get the water for all those houses? The Colorado River is over subscribed. One of the worst droughts in history is going on there in Arizona right now. And those of us up here in the Rust Belt just cemented a deal so they cannot steal water from the Great Lakes. Oh well, in 20 years it will all be part of Mexico once again, anyway.

Keep up the great work!

S.B.

==================================================

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Tuesday 17 January 2006

Bankruptcy Law Backfires Already

The Washington Post is reporting Bankruptcy Counseling Law Doesn't Deter Filings.

At the time I proposed it would backfire. The way to get around the means test is to be incredibly in debt and or lose a job and or be so far under that bankruptcy is the only option. That means test will likely ENSURE that those filing wait until they are damn sure they can not possibly meet the means test, racking up more bills in the meantime.

Those few that do opt into a pay back plan will be all the more careful to never rack up credit card debt again, barring of course a medical disaster or other emergency. This bill, designed to make people debt slaves forever, was doomed from the start.

Everyone seemed to expect bankruptcies to fall off a cliff after the October dealine under the old rules. Well the number initially plunged but comparing the rate to a period right after Katrina and right before a legal change is not exactly right. The important point is that it only took a few weeks for the rate to rise from 3,600 a week to 5,000 a week.

That is a lot of distress.

And I confidently predict it will get a lot worse too.

Following is just one reason:

The Orange County Register is reporting late property tax payments.

Does anyone think those are "one day" sales?

Not me. Check out the Inman News January report card:

"There are now nearly 200,000 more unsold new homes under construction than there were just five years ago. Rapidly rising sales have masked the surge in construction. Most analysts focus on the months of new-home supply, which is shown below. Since hitting a low of 3.5 months of supply in the summer of 2003, this number has gradually increased to its current value of 4.9 months, its highest value since December 1996. While 4.9 months of supply is not concerning because the figure remains so low by historical standards, the months of supply calculation is held down by the high level of sales. If sales slow even a little, the months of supply figure will surge, as it did in 1990. The total number of unsold new homes is shown in the purple line below. There were 503,000 unsold new homes in November 2005, compared with 305,000 in November 2000."

Here is the lethal mix:

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Three months after a new bankruptcy law took effect, the overwhelming majority of debtors seen by credit counseling agencies are filing for bankruptcy instead of using repayment plans envisioned by the law's supporters.Key findings:

The law requires debtors to see credit counselors before they file for bankruptcy protection. It is a prerequisite that banks and credit card issuers hoped would steer consumers away from bankruptcy court and into plans that would allow them to repay debts over a few years.

But so far, that is not happening.

The counseling agencies say most debtors are in such deep financial trouble that they cannot qualify for a debt-management plan.

"Typically, consumers are too far gone when they get to us," said Ivan L. Hand Jr., president and chief executive of Money Management International Inc. (MMI), the nation's largest credit-counseling organization.

That was true during an afternoon spent with MMI credit counselor Lynn Cameron as she advised consumers from a small, gray cubicle in a 150-operator call center in Phoenix last month.

"Bankruptcy is about the only option," Cameron told a Colorado couple whose home was about to be foreclosed upon.

"It doesn't look like you have any alternative at this point," she said on her next call -- with a Maryland family of four with more than $59,000 in credit card debt.

"Bankruptcy looks like a very good option," she repeated an hour later to a disabled 60-year-old with no income and no assets but lots of debts.

In the first 13 weeks after the new law took effect Oct. 17, only 4.5 percent of the 14,907 debtors counseled by MMI had sufficient income to be considered for a plan to pay back debts over a few years. Of those 669 debtors, only 42 have signed up so far for such a debt-management plan.

Financial industry executives, who had pushed for the new law to reduce the record number of bankruptcy cases, say it is too early to tell how well the new credit-counseling requirement is working -- especially because so many consumers rushed to file under the old, less-restrictive law. In the two weeks before the new law took effect, more than 600,000 debtors filed for protection from creditors.

Previously, filings had averaged about 30,000 a week. The number dropped to about 3,600 a week right after the new law took effect, but is now about 5,000 a week and is expected to climb as holiday bills come due.