Annual revisions released Monday show that China's holding of US treasuries is 30% greater than reported just weeks ago.

I am not surprised given that persistent rumors of China dumping treasuries made little mathematical sense from a balance of trade standpoint. Instead, I suggested China was accumulating treasuries via trading desks in the UK. We now see that is precisely the case.

China, the biggest buyer of U.S. Treasury securities, owns a lot more than previously estimated.

In an annual revision of the figures, the Treasury Department said Monday that China's holdings totaled $1.16 trillion at the end of December. That was an increase of 30 percent from an estimate the government made two weeks ago.

China was firmly in the top spot as the largest foreign holder of U.S. Treasury debt even before the revisions. But the big increase in Chinese holdings could ease fears that Chinese investors might begin dumping their U.S. holdings. Such a development could send U.S. interest rates rising. That would slow America's economic recovery and increase Washington's costs for financing the $14.3 trillion national debt.

China and Britain were the countries with the biggest revisions in the new report.

The amount of U.S. Treasury securities held by Britain fell to $272.1 billion in the new report. That's a drop of $269.2 billion from the last monthly report which put the Britain's holdings of U.S. debt at $541.3 billion. The holdings of the two countries often show big revisions when the annual report is released.

The reason for the change is that Chinese investors who purchase their Treasury securities in London are often counted as British investors. The more detailed annual report does a better job of tracking the countries in which investors reside as opposed to the location where investors make their purchases.

Even with the revision, Britain remained the third largest holder of U.S. Treasurys.

Japan had the second highest foreign holdings, totaling $882.3 billion at the end of December. The revision was only slightly below the original estimate.

The total foreign holdings of Treasury debt stood at $4.44 trillion at the end of December, according to the new report. That's up 1.5 percent from the estimate made two weeks ago. About two-thirds of U.S. Treasurys owned overseas are held by foreign governments and central banks.

Thoughts on Dumping Treasuries

Please note the comment in the article: "The big increase in Chinese holdings could ease fears that Chinese investors might begin dumping their U.S. holdings. Such a development could send U.S. interest rates rising. That would slow America's economic recovery and increase Washington's costs for financing the $14.3 trillion national debt."

The odds of China dumping US treasuries are tiny. The last thing China wants to do is put massive upward pressure on the Yuan, and dumping treasuries would likely do just that.

Given that dollars held by foreign central banks earn no interest, governments buy other US assets instead, notably US treasuries. Last year China's bought massive amounts of US treasuries via UK banks or brokers.

Unsustainable Model

Although it is relatively easy to explain what is happening and why, it's also important to know the existing global currency hegemony will eventually collapse because the current model is unsustainable.

Countries cannot run massive deficits forever.

However, a global currency crisis does not necessarily start with the US dollar, nor does a crisis necessarily happen any time soon. A major crisis starting with the Euro, the Yen, the British Pound, or the Yuan is at least as likely, and the timeframe can be months or years away.

Whenever it happens, don't be caught without gold.

A number of sites are commenting on a Bloomberg video in which El-Erian, PIMCO Co-CEO says "Dollar could lose its reserve currency status".

Bloomberg: "Mohammad what does a weak dollar signal to you, a dollar that can't jump up here on a day like we've seen today?"

El-Erian: "It is a warning shot to America that we cannot simply assume flight to quality, flight to safety. That people are starting to worry about the fiscal situation in the U.S. They are starting to worry about the level of debt. They are starting to worry about what they hear about states and municipalities. So, I would take this as a warning shot that we cannot assume that we will maintain the standing of the reserve currency as we have in the past."

Reserve Currency Definition

Before we can debate whether or not the US will lose reserve currency standing, we must first define what it means.

"A foreign currency held by central banks and other major financial institutions as a means to pay off international debt obligations, or to influence their domestic exchange rate."

I accept that definition. Unfortunately Investopedia rambles on with nonsense about the implications: "A large percentage of commodities, such as gold and oil, are usually priced in the reserve currency, causing other countries to hold this currency to pay for these goods."

That sentence is a widely believed fallacy. The reality is no country is obligated to hold dollars to buy goods denominated in dollars.

Currencies are Fungible

Currencies other that illiquid currencies with low or no trading volume (think of Yap Island stones or the Cuban Peso) are fungible. It is a trivial process to switch from one currency to another.

You can buy gold or silver in any country, and I assure you those transactions do not all take place in dollars. Thus, just because a commodity is widely priced in dollars does not mean it only trades in dollars.

That holds true for oil as well.

I keep pointing this out, unfortunately to no avail, that oil trades in Euros right now. There is no selling of Euros to buy dollars on the front causing the oil producers to trade dollars for euros on the back end. The oil states simply sell oil for a price in Euros and then hold Euros in their Forex reserves.

Fact and Fantasy

The first part of what El-Erian said is factual. Here it is again for convenience. "People are starting to worry about the fiscal situation in the U.S. They are starting to worry about the level of debt. They are starting to worry about what they hear about states and municipalities."

Those are true statements. Unfortunately, his "warning shot" regarding reserve currency status is fallacious.

To understand why, let's return to the definition of reserve currency: "A foreign currency held by central banks and other major financial institutions as a means to pay off international debt obligations, or to influence their domestic exchange rate."

Foreign Currency Reserve Factors

Trade Volumes

Trade Deficits

Currency Manipulation

Hot Money

Trade Volumes and Trade Deficit

The US happens to be at or near the top of nearly every country's trading partners. The US runs a trade deficit with most of them. Those trading partners accumulate dollars as a simple function of math. We run a deficit, someone else runs a surplus.

Some wonder why the surplus countries do not buy oil or commodities with their accumulated dollars. OK, what does Saudi Arabia, Iran, or Venezuela do with the dollars then?

Does Iran or Venezuela even hold dollars now? Think of the implications of that answer in light of the widely viewed fallacy that one needs dollars to buy oil.

Regardless, of where the dollars end up, those US dollars will eventually return home. Recall that Dubai tried to buy a US port and China tried to buy Unocal. Both were rejected for security reasons. However, those dollars will return home, with China, Japan, and the oil states buying various US assets.

Currency Manipulation

Most US trading partners do not want their currencies to rise, especially China and Japan.

Consider the Yuan which does not float. To suppress the value of the Yuan, China takes US dollars and exchanges them for Yuan at a pegged rate. China does this hoping to create job and boost exports.

The US calls this currency manipulation and it is. However, it is no more manipulative than Bernanke flooding the markets with US dollars hoping to weaken the US dollar and stimulate growth.

Hot Money

Hedge funds and other speculators have moved money to China banking on currency appreciation.

China needs to maintain currency reserves to allow for the repatriation of those US dollars. Michael Pettis at China Financial Markets points out that most of the hot money inflows into China are done by Chinese businesses that understand how to get around rules and regulations regarding currency inflows.

That argument make perfect sense, but the math remains the same regardless of where the hot money comes from.

Global Beggar-Thy-Neighbor Policies

It is pretty pale to suggest the end of the US dollar as a reserve currency when countries hold dollars as a function of math, then hold still more dollars to suppress their currencies, hoping to keep their exports up to "stimulate growth".

Mathematical Impossibility

Another mathematical relationship says the dollar, the pound, the Yen, and the Yuan cannot all be weak at the same time (relative to each other). Yet that is precisely what every country wants. It's mathematically impossible.

You can see the effect in rising commodity prices.

If commodity prices were a function of the US dollar alone, then they would be rising in US dollar terms alone. Instead there is upward pressure on commodities in all currencies.

At some point the desirability to hoard commodities will peak.

Regarding El-Erian's statement: "I would take this as a warning shot that we cannot assume that we will maintain the standing of the reserve currency as we have in the past"

Zero Hedge quipped:

That's a given - the question however remains, which fiat currency, if any, is willing and ready to step in and replace the USD? With all eyes continuing to be look at the CNY, how long before China finally takes the plunge to find out just who is the real reserve currency in the world?

Will Another Fiat Currency Replace the Dollar?

For starters, Zero Hedge ignored the essential trade deficit math. The US runs a trade deficit, someone else must run a trade surplus.

Second, Canadian dollar and the Swiss Franc do not have enough trading volume. More importantly, there are not enough Canadian Dollars or Swiss Francs to go around. Look at what happened to Iceland when too many plunged into the Icelandic kr�na.

The Canadian and Swiss economies are simply not big enough for them to be global reserve currencies. In regards to the Euro, is Europe in a better fundamental situation than the US? Would it matter even if it was? To answer the second question, please remember trade deficit math.

As for the Yuan, it is complete silliness to suggest the currency of a command-economy dictator-led country that will not even float its currency will be some sort of major reserve currency.

To the extent that China trades with Russia, South Korea, etc., local reserves in varying currencies can happen (and are happening already), but the global significance of it is wildly overstated. The amounts in question are tiny, as a simple function of math.

Will the dollar remain the global reserve currency forever? Of course not. However, it is highly unlikely any of the presumed leading Fiat candidates including the Yuan and the Keynesian wet-dream IMF SDRs (Special Drawing Rights), will take the dollar's place. SDRs are essentially a basket of currencies.

The concept of trading in baskets of currencies backed by nothing is even more ridiculous than the existing setup. People do not buy goods and services in baskets of currencies.

What can replace the dollar?

Gold, or a mechanism like gold that would impose a hard restrictions on perpetual deficits is what its takes to restore sanity. However, we may not see a significant move towards gold until there is a massive currency crisis or revolt against fiat currencies in general, not just the US dollar.

Libyan rebels now hold about 80% of the country. France is sending an airlift of medical supplies, including doctors and nurses to aid the rebels. Think anything else might be in those planes?

Regardless, Qaddafi is holed up in Tripoli with options growing smaller by the day. The only country that might take him is Venezuela. Why anyone would take him is beyond me.

An international campaign to force Col. Muammar el-Qaddafi out of office gathered pace on Monday as the European Union adopted an arms embargo and other sanctions, as Secretary of State Hillary Rodham Clinton bluntly told the Libyan leader to surrender power �now, without further violence or delay.�

Germany proposed a 60-day ban on financial transactions, and a spokeswoman for Catherine Ashton, the European Union�s foreign policy chief, said that contacts were being established with the opposition.

Italy�s foreign minister on Sunday suspended a nonaggression treaty with Libya on the grounds that the Libyan state �no longer exists,� while Mrs. Clinton said the United States was reaching out to the rebels to �offer any kind of assistance.�

France said it was sending medical aid. Prime Minister Fran�ois Fillon said planes loaded with doctors, nurses and supplies were heading to the rebel-controlled eastern city of Benghazi, calling the airlift �the beginning of a massive operation of humanitarian support for the populations of liberated territories.�

Across the region, the tumult that has been threatening one autocratic government after another since the turn of the year continued unabated. In Yemen, protests drove President Ali Abdullah Saleh to make a bid for a unity government, but the political opposition rapidly refused. An opposition leader, Mohamed al-Sabry, said in a statement that the president�s proposal was a �desperate attempt� to counter major protests planned for Tuesday.

In Bahrain, protesters blocked access to Parliament, according to news agencies. In Oman, whose first major protests were reported over the weekend, demonstrations turned violent in the port city of Sohar, and spread for the first time to the capital, Muscat.

Hundreds of Omani protesters gathered in the city of Sohar for a third night, demanding that the government open talks on their demands for more jobs, higher pay and more representative political institutions.

Khaled Maqbuli, a leader of the protest, called on the demonstrators at a roundabout in the center of Sohar, north of the capital, Muscat, to stay peaceful and avoid confrontation with the army and the police. Two people were killed, several wounded and a supermarket set on fire over the past two days.

�We are peaceful, we have demands, we are not saboteurs,� Maqbuli, 26, said through a loudspeaker. �We want the government to send civilian people to discuss our demands; we have nothing to say to the military.�

Sultan Qaboos Bin Said, the country�s ruler since 1970, �has received the demands of the citizens in all the provinces and is giving them his attention,� state television reported.

If governments could easily create jobs they would. Look no further than the US for proof. Only private enterprise can create jobs, at least lasting ones.

Governments can only take wealth from one place and distribute it elsewhere, by taxation, by force, or by the hidden tax of inflation that comes from printing money. When the stimulus ends, so do the jobs, except the bureaucratic ones, where massive pension problems and needless bureaucrats remain.

The strength in China�s January trade data was absolutely remarkable. Going back to 2000, the level of unadjusted exports or imports in a January month has never exceeded the level in the immediately prior December: until now. There are deep-seated seasonal reasons why this just shouldn�t happen - and history had never offered an exception to the rule. So, clearly, seasonally adjusted month-on-month growth was huge - around 12% for exports and 16% for imports. Iron ore import volumes were a monthly record by almost 7%. Sure, global manufacturing had a strong end to the year and business surveys had a respectable January, but this sort of implied demand is bordering on ridiculous. While three consecutive months of triple digit growth in imports to the special economic zones through Q4 argue the export numbers should not be a total surprise (at least on the supply side, never mind who the customers are), we remain astonished by the import surge.

Yes, commodity prices rose and some public and private discretionary inventory building ahead of the lunar new year was likely underway, but neither factor goes all that far in explaining the level of apparent demand. Getting away from levels and getting back to growth, at 51%yr imports are as strong as they were in the first half of 2004, when the authorities saw fit to clamp down on out of control heavy industrial investment, overall fixed investment began the year up 53% and 24 of 31 provinces experienced power shortages as an overloaded grid strained under the pressure. Is that a good description of the current climate? No, not really, but to say that the economy has good momentum opening the year would be an egregious understatement.

?So, the Chinese economy is expanding at a rapid pace � for now. However, the imbalances that have emerged in the policy induced recovery phase have not disappeared. In fact, they have been inflamed. When real estate policy began to be tightened in the first half of 2010, the volume of sales moved broadly sideways (with regional variation), but the volume of new starts continued to rise .

The implications of this are many. One, bringing these projects to completion will generate very significant demand for raw and intermediate materials. This should keep commodity markets well supported in coming months - even if a pull-back from extraordinary January import levels must be assumed, and the fact that base metals prices are extremely elevated already. But the stronger implication is that once these starts do reach completion it seems extremely unlikely that the level of sales will be high enough to comfortably absorb the new supply. That implies that the developer industry will run into some trouble later this year and into early 2012 � and that will impact on activity levels in the construction sector, with predictable flow-on effects for upstream industries inside China and out.

Estimating a precise lead time between starts and completions is not easy. The private construction cycle is young enough that it has yet to establish firm �rules of thumb� for forecasters to adopt. Chinese housing ownership reforms date back to just 1998 and the explosion in private sector housing activity dates to only 2003. We have a single national downturn to ponder (late 2008) in addition to the Shanghai experiment of 2004/05. While the cycle does appear to be settling into more of an established groove, we are not at a point where we can be confident about the leads and lags. Our best efforts suggest that a lead period of between 1� and 2 years is a reasonable if imprecise guide. As the surge in starts dates back to the middle of 2009, the first �cluster� of completions should be hitting the market in physical form later this year, and in �off-theplan� form somewhat earlier. But the post-April rise in starts is a story for early-mid 2012. Where will sales demand be at this time against a backdrop of monetary tightening? Not high enough.

It should be emphasized that we are talking about new supply coming to market. Secondary stock is to be added to the amount of housing available for sale. When the volume of sales fell below completions in late 2008 (Chart 2) developers were forced to discount aggressively to offload their properties. In the absence of a supportive policy shift as part of the second stimulus package, realised prices could have fallen by 20-30%, essentially consuming the entire margin rumoured to be enjoyed by the luxury development sector. The policy response should events play out as expected is a vitally important question. On the one hand, history argues that the �Wen put� (an analogue of the legendary �Greenspan put�) will again be exercised, thereby sparking another wave of subsidised housing speculation and downstream demand for the heavy industrial sector. On the other, the administration�s oft-stated and pragmatic desire to tackle housing affordability concerns, and their desire to ignite the latent consumption impulse, might argue for a very public sacrifice of the developers. Taken together with the current focus on inflationary risks � both immediate and medium term � and a disinflationary trend emanating from residential real estate doesn�t appear to be wildly inconsistent with the broader aims of policy. Whatever balance the policymakers strike, the implications will resonate far afield.

A satirical YouTube clip mocking Col. Muammar el-Qaddafi�s megalomania is fast becoming a popular token of the Libya uprising across Middle East. And in an added affront to Colonel Qaddafi, it was created by an Israeli living in Tel Aviv.

Noy Alooshe, 31, an Israeli journalist, musician and Internet buff, said he saw Colonel Qaddafi�s televised speech last Tuesday in which the Libyan leader vowed to hunt down protesters �inch by inch, house by house, home by home, alleyway by alleyway,� and immediately identified it as a �classic hit.�

�He was dressed strangely, and he raised his arms� like at a trance party, Mr. Alooshe said in a telephone interview on Sunday. Then there were Colonel Qaddafi�s words with their natural beat.

Mr. Alooshe spent a few hours at the computer, using Auto-Tune pitch corrector technology to set the speech to the music of �Hey Baby,� a 2010 electro hip-hop song by American rapper Pitbull, featuring another artist, T-Pain. He titled it �Zenga-Zenga,� echoing Col. Qaddafi�s repetition of the word zanqa, Arabic for alleyway.

Mr. Alooshe said he was a little worried that if the Libyan leader survived, he could send one of his sons after him. But he said it was �also very exciting to be making waves in the Arab world as an Israeli.�

As one surfer wrote in an Arabic talkback early Sunday, �What�s the problem if he�s an Israeli? The video is still funny.� He signed off with the international cyber-laugh, �Hahaha.�

In Shanghai and Beijing, signs of political unrest are starting to brew. In response, China has clamped down on internet access, banning search words, even names of countries associated with unrest.

For now, police have things under control with a huge display of force relative to the size of the protests. The key words are likely "for now".

Police and security officials displayed a massive show of force here and in other Chinese cities Sunday, trying to snuff out any hint of protests modeled on the uprisings in the Middle East. In Shanghai, several hundred people trying to gather were dispersed with a water truck.

Officials have used state-run media outlets to dismiss any comparisons with China while at the same time stepping up public comments on the need to address "social conflict" and to tackle problems such as the growing income disparity between the rich and poor. They have also detained a number of activists and human rights lawyers, blocked Internet search terms considered sensitive, such as "Egypt," "Tunisia" and even U.S. Ambassador Jon Huntsman Jr.'s Chinese name. And they have issued warnings to foreign journalists to be mindful of reporting restrictions.

A previously unknown group has used an overseas-based Chinese language Web site to call for a series of peaceful, silent protests, named "jasmine rallies" after the Tunisian uprising, on consecutive Sunday afternoons in cities across China. The rallies were called for heavily trafficked commercial areas, public squares and parks, ostensibly so silent protesters could blend in with ordinary passersby to avoid arrest.

However, police on Sunday were out in huge numbers in Beijing, Shanghai and other cities at the sites where the rallies were supposed to take place.

At the Wangfujing protest site in Beijing, a foreign journalist shooting video for a news agency was reportedly punched and kicked in the face by plainclothes Chinese security officers who confiscated his camera. The Foreign Correspondents Club of China reported that more than a dozen other journalists were roughed up at the site.

"I came here today to see how people protest against the government, which is corrupt and rules in an authoritarian way," said a 71-year-old man, who asked that only his family name, Cao, be used. "Democracy is the trend in the world. No country in the world can be an exception to the process."

Another man, named Xia, 64, said there were about 400 to 500 people gathering at People's Square when he arrived around 1 p.m., but they were dispersed by the spray from the water truck. He said he would keep returning to try to protest because he was already in his 60s and not afraid.

On Sunday, Premier Wen sat for two hours for an Internet chat, with the Xinhua news agency and the central government's Web site, www.gov.cn, addressing common complaints and answering questions submitted online. It was Wen's third such Internet chat session, coming just before the March opening of the National People's Congress, China's nominal legislature.

In the session, Wen discussed the problem of corruption, following the recent firing for "discipline violations" of Liu Zhijun, the minister of railways and the top official in charge of China's rapidly expanding high-speed rail development.

Wen also said the government was adjusting its rapid growth targets to an average of 7 percent for the next five years -- and to make sure the growth was balanced and wealth more evenly distributed.

Police Head Off Protests, Premier Vows to Tackle Corruption, Inflation

Chinese Premier Wen Jiabao pledged to punish abuse of power by officials and narrow the growing wealth gap as police blanketed Beijing and Shanghai to head off planned protests inspired by revolts in the Middle East.

The root of corruption lies in a government that has too much unrestrained power, Wen said in a two-hour online interview with citizens today. He promised to curtail food costs and tackle surging property prices. Wen also cut economic growth targets and said the government would focus on ensuring the benefits of expansion were more evenly distributed.

Wen�s comments came as hundreds of police deployed in Beijing and Shanghai at the site of demonstrations called to protest corruption and misrule. At least seven people were bundled into police vans near Shanghai�s People�s Square, while in Beijing several foreign journalists were forcibly removed from the Wangfujing shopping district.

�The new five-year plan will be more about quality of growth,� said Kevin Lai, a Hong Kong-based economist at Daiwa Capital Markets. �The government is going to pay more attention to sustainable growth, environment, better distribution of income, rather than pure GDP pursuit.�

An August report by Zurich-based Credit Suisse AG put income inequality levels in China at levels not seen outside of sub-Saharan Africa. High food prices, unemployment and anger over corruption helped spark the protests that toppled Tunisian President Zine El Abidine Ben Ali, Egypt�s Hosni Mubarak and fueled rebellion against Libya�s Muammar Qaddafi.

An open letter on the U.S.-based website Boxun.com [Mish Note: Website is in Chinese] called for people to gather in at least 27 sites around the country from Tibet to Manchuria for �jasmine� rallies, named after the uprising last month in Tunisia. �Come out and take a stroll at two o�clock on Sundays to look around,� the letter said.

In Shanghai, at least 23 police vehicles were stationed around Shanghai�s Peace Cinema in the shopping area of People�s Square. Police in Beijing, which included paramilitary units and patrols with Rottweiler and German Shepherd dogs, forcibly removed several foreign journalists from Wangfujing Street at about 2:45 p.m. Police were stationed at every entrance to Wangfujing today.

�You see how the police try to control the crowd? They spend so many resources on this, yet why does the government do so little to improve people�s livelihoods?� said a 72-year-old retired car mechanic in Shanghai, who didn�t want to be named because he feared being detained.

Did you note the irony in Premier Wen Jiabao's statements? "The root of corruption lies in a government that has too much unrestrained power", yet the government busts the heads of journalists, blocks internet access, and refuses to let people gather. Finally, the Chinese government bureaucrats plan damn near everything, and the economy is clearly overheating.

If that is not the epitome of "too much unrestrained power", what is?

Muammar el-Qaddafi still has control of Tripoli but hardly anything else. The United Nations Security council has imposed sanctions and is investigating war crimes. However, the security council did not impose a no-fly zone that some wanted.

In Oman, police fired teargas at protesters and two were shot dead when demonstrators tried to storm a police station. In response, the sultan changed six ministers in "the public's interest".

ZAWIYA, Libya � In this city 30 miles west of Tripoli, hundreds of people rejoiced in a central square on Sunday, waving the red, black and green flag that has come to signify a free Libya and shouting the chants that foretold the downfall of governments in Tunisia and Egypt: �The people want to bring down the regime.�

Rebels, in control of the city, had reinforced its boundaries with informal barricades, and military units that had defected stood guard with rifles, six tanks and anti-aircraft guns mounted on the backs of trucks. In the central square here, a mosque was riddled with enormous holes, evidence of the government�s failed attempt to take back this city on Thursday. Nearby lay seven freshly dug graves belonging to protesters who had fallen in that siege, witnesses said.

Proving how close opposition control has come to the capital, where Col. Muammar el-Qaddafi maintains tight control, the confidence of the demonstrators in Zawiya was remarkable, all the more so because it was witnessed as part of the official tour for international journalists that Colonel Qaddafi�s government organized. The public relations effort, apparently intended to show a stable Libya to the outside world, appeared to backfire, as a tour of Tripoli had on Saturday.

Instead, the tour, whose minders were forced to wait at the city�s outskirts, showed a nation where the uprising had reached the capital�s doorstep, underscoring a growing impression that the ring of rebel control around Tripoli was tightening. But in a sign that the fight was far from over, armed government forces were seen massing around the city.

Hillary Rodham Clinton, the secretary of state, said Sunday before departing for Geneva that the United States was �reaching out to many different Libyans who are organizing in the east� but said it was too soon to recognize a provisional government.

Security Council Calls for War Crimes Inquiry

Qaddafi's options are rather limited at this point. He can stay and fight to the last drop of his blood, he can flee to Venezuela, one of the few countries that would take him, or if he gives up, he likely faces a war crimes tribunal, assuming his own military does not take him out.

The United Nations Security Council voted unanimously on Saturday night to impose sanctions on Libya�s leader, Col. Muammar el-Qaddafi, and his inner circle of advisers, and called for an international war crimes investigation into �widespread and systemic attacks� against Libyan citizens who have protested against the government over the last two weeks.

The vote, only the second time the Security Council has referred a member state to the International Criminal Court, comes after a week of bloody crackdowns in Libya in which Colonel Qaddafi�s security forces have fired on protesters, killing hundreds.

Also on Saturday, President Obama said that Colonel Qaddafi had lost the legitimacy to rule and should step down.

The Security Council resolution also imposes an arms embargo against Libya and an international travel ban on 16 Libyan leaders, and freezes the assets of Colonel Qaddafi and members of his family, including four sons and a daughter. Also included in the sanctions were measures against defense and intelligence officials who are believed to have played a role in the violence against civilians in Libya.

The sanctions did not include imposing a no-fly zone over Libya, a possibility that had been discussed by officials from the United States and its allies in recent days.

The resolution also prohibited all United Nations member nations from providing any kind of arms to Libya or allowing the transportation of mercenaries, who are believed to have played a part in the recent violence. Suspected shipments of arms should be halted and inspected, the resolution said.

Two Oman Protesters Shot Dead

Protests and violence are unusual in Oman, a country where political parties are outlawed. Nonetheless, Yahoo! News reports Two protesters shot dead in Oman

Omani police shot dead two demonstrators with rubber bullets on Sunday, a security official said, as the deadly wave of protest rocking the Arab world spread to the normally placid pro-Western sultanate.

Five people were also wounded when security forces opened fire on the demonstrators who tried to storm a police station, the official said.

"Two were killed after being shot with rubber bullets as protesters attempted to storm a police station" in Sohar, some 200 kilometres (125 miles) northwest of Muscat, the official said, requesting anonymity.

In an apparent move to appease demonstrators, Qaboos on Saturday announced an increase in the monthly allowance for students at universities and vocational schools.

ONA said he ordered a raise in the allowance of between 25 and 90 Omani rials ($65 to $234) to "achieve further development and... provide a decent living for his people."

He also ordered the creation of a consumer protection bureau, and was looking into opening cooperatives, it said.

Earlier this month, Oman raised the minimum wage for an estimated 150,000 private sector employees from $364 to $520 a month.

Six Oman Cabinet Ministers Changed in Public Interest

Oman's Sultan Qaboos bin Said reshuffled his cabinet on Saturday, changing six ministers in "the public's interest," one week after a rare protest calling for political reform.

The cabinet changes came as 500 protesters demanding democracy and jobs blocked traffic and broke street lights in the largest industrial city Sohar. Protests are rare in Oman, a small Gulf country where political parties are banned.

In Sohar, protesters blocked cars and shoppers at a mall in the city to demand that the Gulf Arab state's elected advisory body be given legislative powers, witnesses said.

Protesters chanted: "We want long-term corrupt ministers to go!" "We want the Shura Council to have legislative powers!" "We want jobs!" and "We want democracy!"

"It has been going on for hours now. They are now at the Globe Roundabout blocking traffic," said Mohammed Sumri, a resident. The police did not intervene, residents said.

The voting is over in Ireland and in this writer's eyes, quite anticlimactic. Fianna Fail, the party that agreed to enormously unpopular austerity measures to bail out UK, German, French and US banks, was blasted to smithereens. The vote was both expected and well deserved.

The real fun begins now, and it is not at all certain what that outcome is. My choice is for default, but I do not get to vote. However, if common sense prevails, the EU and ECB is in for a rude shock.

Ireland's new government on a collision course with EU

Exit polls and early tallies from Ireland's general election heralded political annihilation for Fianna Fail (FF), the party which has ruled Ireland for more than 60 years of the Irish Republic's eight decades of independence.

The unprecedented and historic defeat, Fianna Fail's worst result in 85 years, makes the Irish government the first eurozone administration to be punished by voters in the aftermath of the EU's debt crisis. Voter turn-out was exceptionally high at more than 70 per cent, indicating public anger at the government and the EU.

Late last year, Ireland was forced to accept a �72 billion EU-IMF bailout to cover huge public debts that were ran up to save failed Irish banks.

The bail-out was designed to prevent financial contagion that threatened the existence of the euro, but according to economic forecasts, the cost of servicing Irish bank debt and the EU-IMF bank loans will consume 85 per cent of Ireland's income tax revenue by 2012, a burden that a majority of voters find intolerable.

Brian Cowen, the Irish Prime Minister and Fianna Fail leader, who stood down last month rather than face furious voters, was also pressured into implementing a savage �13billion austerity programme of tax rises and spending cuts drawn up by the EU.

The cost of the EU-IMF bailout in extra taxes for an average Irish family has been estimated at over �3,900 a year. Other deeply unpopular measures include controversial reductions to the minimum wage, unprecedented cuts to public services and 90,000 jobs losses in a country where unemployment is already running at almost 14 per cent.

In Dublin, Fianna Fail won just eight per cent of the vote in an electoral decimation that called into question the future of previously unassailable politicians such Brian Lenihan, the Irish finance minister.

"However bad people thought it would get for Fianna Fail, nobody thought it would get this bad," said Michael Marsh, professor of political politics at Trinity College Dublin. "That is highly significant."

Based on anger and some preliminary polls, I thought FF would get about 10-12% of the vote. By that measure Fianna Fail did as well as could have been expected except in Dublin.

Unfortunately, Brian Lenihan, one of the complete fools behind the Irish sellout to the EU, appears likely to retain his seat. However, he is burnt toast as Finance Minister. Please see Lenihan battles the tears as he claims fourth seat for details.

Returning to The Telegraph ...

Enda Kenny, Fine Gael's leader, will later on Sunday, start to form a new government, almost certainly with Labour, after full election results under Ireland's complicated PR system come through.

Both Mr Kenny and Eamonn Gilmore, Labour's leader, have promised Irish voters that they will renegotiate the EU-IMF austerity programme to reduce the burden for taxpayers and to force financial investors to shoulder some of the bank debts currently paid out of the public purse.

At a summit of centre-right EU leaders in Helsinki next Friday, Mr Kenny will use his position as Ireland's new Prime Minister to beg the German Chancellor, Angela Merkel, and French President, Nicolas Sarkozy, for concessions ahead of an emergency March 11 Brussels summit to restructure the euro zone.

But neither the two European leaders nor the European Central Bank or EU will permit any substantial changes, despite the huge popular Irish revolt against the bailout.

Chancellor Merkel will tell Mr Kenny that if he wants to reduce the high, punitive 5.8 per cent interest rate charged on EU loans then Ireland will have to give up its low corporate tax rates - a measure regarded as vital to Ireland's recovery and one of the few economic policies it has not yet handed over to Brussels or Frankfurt.

The new Irish premier will also be warned that there is no question of forcing privately-owned financial institutions to assume Ireland's �85 billion bank debts because the resulting market panic would spread to Germany and France, tearing the euro single currency apart.

As Irish voters headed for the polling booths on Friday, the European Commission bluntly declared that the terms of the EU-IMF bailout "must be applied" whatever the will of Ireland's people or regardless of any change of government.

"It's an agreement between the EU and the Republic of Ireland, it's not an agreement between an institution and a particular government," said a Brussels spokesman.

A European diplomat, from a large eurozone country, told The Sunday Telegraph that "the more the Irish make a big deal about renegotiation in public, the more attitudes will harden".

"It is not even take it or leave it. It's done. Ireland's only role in this now is to implement the programme agreed with the EU, IMF and European Central Bank. Irish voters are not a party in this process, whatever they have been told," said the diplomat.

Arrogance and Gall of the EU

Ireland, not the EU is in charge here. The opening salute from Kenny should not be to ask for EU concessions but to simply say "Go to Hell" or more politely to offer 1 cent on the dollar for debt.

That will set the proper tone for serious negotiation, and it is something I have been saying for many months.

Calls for a Vote

Dessie Shiels, an independent candidate in Donegal, said: "People have not been given the basic right of deciding whether or not they should have their taxes increased in order to repay bondholders who have lent to the banks."

David McWilliams, an economist and former official at the Ireland's Central Bank, has led calls for a popular vote under Article 27 of the Irish constitution, which requires on a matter of "such national importance that the will of the people ought to be ascertained".

"We have to re-negotiate everything," he said. "Obviously, the first way to do this is to make them aware that if they force us to pay everything, we will default and they will get nothing. So they had better get a little bit of something, than all of nothing. To make this financial pill easier to swallow, we must take the initiative politically. We can do this via a referendum.

"If the Irish people hold a referendum on the bank debts now, we can go to the EU with a mandate from the people which says No. This will allow our politicians to play hard-ball, because to do otherwise would be an anti-democratic endgame."

Declan Ganley, the Irish businessman who led the 2008 No vote to the Lisbon Treaty, said Ireland must "have the balls" to threaten debt default and withdrawal from the single currency.

"We have a hostage, it is called the euro," he said. "The euro is insolvent. The only question is whether Ireland should be sacrificed to keep the Ponzi scheme going. We have to have a Plan B to the misnamed bailout, which is to go back to the Irish Punt."

Calling for a vote is actually a very good idea. It would remove the stigma of Kenny saying "Go to Hell". Instead the people of Ireland can vote to tell the EU to "Go to Hell".

Other than outright default, putting the decision to a vote is the only thing that makes any sense given the stubborn arrogance of the EU.

Onerous Terms Cannot and Will Not be Honored

It is beyond stupid to demand terms so onerous they cannot possibly be paid back. Martin Wolf, writing for the Financial Times feels the same way.

This is not one, but three, crises: an economic collapse; a financial implosion; and a fiscal disaster. On the first, given the fall in demand and the need for fiscal contraction, prospects for recovery depend heavily on exports. On the second, the direct costs of recapitalising the system are set to be around 36 per cent of GDP, according to Goodbody stockbrokers. On the last, according to the IMF, general government debt could be 123 per cent of GDP by 2014. A little over a third of this increase in the public debt ratio would then be a direct result of recapitalising the banks.

Such a crisis is beyond the ability of Ireland to manage without financial collapse and sovereign default.

Apart from the Armageddon of a sovereign default, two partial escapes exist. The more trivial would be a reduction in the rate of interest on Ireland�s borrowing: a 1 per cent reduction in the rate of interest would save the state 0.4 per cent of GDP a year. That would be a small help, at least. A more valuable possibility would be a writedown of existing subordinated and senior bank debt, which currently amounts to �21.4bn (14 per cent of GDP).

The ECB and the other members of the European Union have vetoed this idea, fearful of contagion. Indeed, the assistance package was partly to prevent just such an outcome. Yet the idea that taxpayers should bail out senior creditors of massively insolvent banks at such risk to the solvency of their state is both unfair and unreasonable. If the rest of the EU is determined to protect senior creditors, it should surely share in the cost of doing so. Why should the taxpayers of the borrowing country pay all? The new Irish government should make this point firmly.

Key Question

Changes in interest rates are meaningless, so would trivial, symbolic writedowns.

Wolf asked the key question I have been asking for months: Why should the taxpayers of the borrowing country pay all?

The answer is they shouldn't. Moreover I doubt they can. It would wreck the Irish economy to do so. If the EU breaks up over this, well that is the EU's problem more than it is Ireland's.

It is high time banks, not taxpayers bear the brunt of stupid lending decisions. There is no better time than the present to send that message, and the best way to do that is have the voters of Ireland decide.

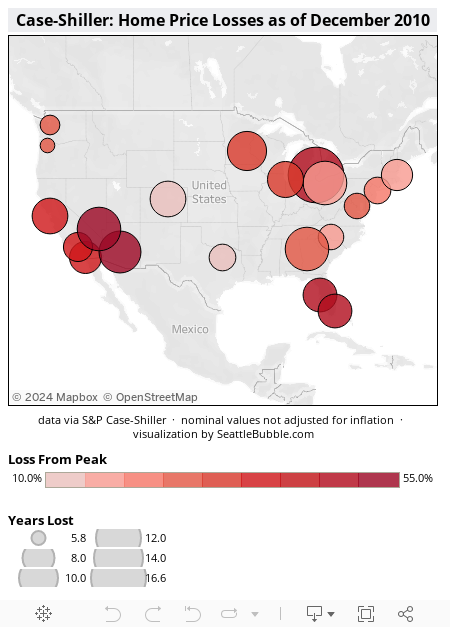

Reader Ron is from the Midwest and asks about Phoenix...

"I am very interested in the Phoenix housing data, however given the commentary below I cannot tell either context or time frame. Is Phoenix improving or declining? I cannot tell from your article. Can you elaborate in terms and time frame that would explain?"

Hello Ron

Phoenix may easily be close to the bottom given that massive drop.

However, I would not expect significant appreciation for years even IF Phoenix is at the bottom. That holds true for any bottoming area. I think parts of Florida have probably bottomed as well, but prices could easily stagnate for a decade.

In general, the last bubble is not reblown for decades. Look at the Nasdaq or better yet, the Nikkei.

If you are thinking of moving to and living in Phoenix, I believe the worst of the decline is over. However, if you are thinking about the rental market, you need to be very careful if you do not know what you are doing.

I own three residential home properties in Orlando that I bought in 2006, and obviously over held them and they are now all worth half the price. I have had many problems with leasing them out due to many people moving in making the place a mess and leaving due to personal financial problems!

I cannot figure out what to do with the homes now because the options are to lose half my investment or ruin my credit. I do not like either option.

Recently I have been contacted by a gentleman that lives in the area and he found 3 year lease to own (option to buy) tenants for two of my homes, I read over the contract and they are very attractive, 3 years contracted tenant, and an option price at the end of three years at the price of the peak in 2007 or double the price of the home now.

Is this a scam for me as the owner or is this a scam for the tenant, or both ways? Let me know if you know anything about this?

Stuck-in-Florida

Hello Stuck...

I cannot answer your question directly but I may be able to help.

For starters, I am suspicious of "offers to help". Moreover, I do not know Florida law or any specific Florida pitfalls, nor can I (or would I even if I could, attempt to sort out a legal contract for anyone).

Secondly please note what I said to the potential Phoenix buyer above. Even IF this is the bottom, do not expect rapid appreciation, perhaps any appreciation. In real (inflation adjusted returns), I expect real estate to be a poor investment for as long as a decade.

Do you really want to be a landlord?

Even if you do, my advice is simple and easy to understand: Before you sign anything or do anything please consult with an attorney for your state.

You may wish to consider walking away, or you may want to go ahead if an attorney reviews what you have in mind. Again, I am very suspicious of "offers to help". Perhaps that offer is not a scam, perhaps it is.

I do not have legal contacts for many states. In fact, I happen to have a contact for precisely one state. That state just happens to be Florida.

Please read Before Walking Away Consult An Attorney for information about walking away and the name of a Florida attorney specializing in real estate problems.

Tell him Mish sent you. I get nothing out of this. I am just trying to help. Good luck to you.

Almost 200 German economics professors have signed a declaration rejecting current proposals to resolve the eurozone debt crisis, instead calling for a way for distressed countries to declare bankruptcy.

More than 200 professors were invited to sign the document, and 189 did so, including prominent figures such as Manfred Neumann of the University of Bonn and Justus Haucap of the University of Duesseldorf, both in western Germany.

Instead of the collective support mechanism set up last year that could be made permanent in a modified form from 2013, the economists argued it would be better to let countries restructure their debts.

"Restructuring allows the countries concerned to reduce their debt and start over," said the economists.

The solution being mulled at present and likely to be approved by European leaders next month would amount to "a permanent guarantee" of some countries' debt, with "very serious consequences," they added.

The signatories also doubted the effectiveness of measures to reinforce the competitiveness of weaker eurozone countries and control members' public finances owing to the European Union's "limited firepower."

The document was published as lawmakers from Chancellor Angela Merkel's ruling coalition sent her a clear message ahead of negotiations on a permanent EU rescue plan to take place in Brussels.

The German deputies said the future European Stability Mechanism should not be allowed to buy eurozone government debt, as the European Commission and European Central Bank would like.

Those 189 academics simply want the ECB to admit that the debt owed by Greece, Ireland, Spain, Portugal, cannot possibly be paid back. What cannot be paid back, won't, and pretending that it will just makes problems worse. It is refreshing to see a large group of academics on the right side of an economic issue.

Axel Weber, once heir apparent to ECB presidency to replace Jean-Claude Trichet, resigned as president of the German central bank over the issue of the ECB buying sovereign debt. He did not want the ECB to buy debt, most of the rest of the ECB did.

Academics in Germany are disregarded even though they make economic sense. Keynesian and Monetarist academics in the US make no sense but are revered.

Tim Ellis at the Seattle Bubble blog sent me an email along with an interesting map of data on Case Shiller 20 metropolitan housing market index in Tableau form. Please give the table a few seconds to load.

HousingPanic, a particularly vitriolic BubbleBlog � which is saying something � asks: Realistically, how overvalued are Phoenix home prices?

Obviously, I consider this a profoundly silly question, but to lurk among the BubbleBloggers and their seething commentariat is to acquire an education in a slice of America invisible from this side of the sewer gratings. Notwithstanding the idiotic economic analysis, which is really no worse than the static-market fallacies paraded as profundities in the pages of the Arizona Republic, these sites � and not just HousingPanic � are infested with a cult-like fever to inflict suffering � at second hand, to be sure � on people who are in fact guilty of nothing except failing to have drunk the BubbleBlogger KoolAde.

That�s all one. I don�t care. The whole of the last century was dominated by the bad behavior of viciously angry wretches, but look where it got them. The BubbleBloggers will someday bawl balefully in private, but they will never, ever admit that they have been very publicly very foolish. You will know and I will know and in the secret chambers of their hearts they will know they were wrong all along. But as long as you don�t hold your breath waiting for that contrite admission of error, you should be fine.

Here�s where I do start to care. Whenever the subject of Phoenix comes up in a BubbleBlog, the assembled Brown Shirts pile on, for whatever reason. ...

Which brings me back to HousingPanic�s question. We keep our own home sales price statistics, so we have no doubt that values are down from their high in December. How much? Right now, about 4%. Could they go lower? Certainly. Will they drop by the huge amounts HousingPanic and his flying monkeys seem to yearn for? This seems very unlikely.

What seems much more likely is that Phoenix will recover from the hangover of last year�s buying binge and get back to a steady rate of growth � historically 6% a year. The reason this should happen is very simple: Population growth. ...

Greg Swan, super Phoenix bull drones on with 21 preposterous reasons why Phoenix will not crash. All of his reasons were rebutted at the time and in detail by myself and others so many times and in so many places, I could fill up pages listing them.

To name a single name, Professor Piggington was among the first with a complete analysis, not of Phoenix per se, but a thorough, and sound analysis why the population argument did not hold up.

The first chart above is mine. I added the annotations on the second chart, created by Professor Piggington.

Here is my favorite quote at the time.

Gregory J. Heym, the chief economist at Brown Harris Stevens, is not sold on the inevitability of a downturn. He bases his confidence in the market on things like continuing low mortgage rates, high Wall Street bonuses and the tax benefits of home ownership."It is a new paradigm" he said.

We now have the truth. It was not a "new paradigm". Price-to-rent and price-to-wage matters.

Doug Swan "Notwithstanding the idiotic economic analysis, which is really no worse than the static-market fallacies paraded as profundities in the pages of the Arizona Republic, these sites � and not just HousingPanic � are infested with a cult-like fever to inflict suffering � at second hand, to be sure � on people who are in fact guilty of nothing except failing to have drunk the BubbleBlogger KoolAde. ... Right now, [prices are about 4% lower]. Could they go lower? Certainly. Will they drop by the huge amounts HousingPanic and his flying monkeys seem to yearn for? This seems very unlikely."

Who's the Flying Monkey?

It was Greg Swan's self-serving economic analysis and hype (and tens of thousands of other Realtors as well) that helped lure dumb speculators into "can't lose" Phoenix. Prices are now 54.7% off the peak in June 2006.

Greg Swan called housing bears "flying monkeys" right as his area peaked. I believe congratulations are in order. It's not easy to be that boldly inept.

Addendum:

Reader Ron asks ...

"I am very interested in the Phoenix housing data, however given the commentary below I cannot tell either context or time frame. Is Phoenix improving or declining? I cannot tell from your article. Can you elaborate in terms and time frame that would explain?"

Hello Ron

Phoenix may easily be close to the bottom given the drop. However, I would not expect significant appreciation for years even IF it is at the bottom. That holds true for any area bottoming. I think parts of Florida have probably bottomed as well, but prices could easily stagnate for a decade.

In general, the last bubble is not reblown for decades. Look at the Nasdaq or better yet, the Nikkei.

If you are thinking of moving to and living in Phoenix, I believe the worst of the decline is over. However, if you are thinking about the rental market, you need to be very careful if you do not know what you are doing.

You nailed it on the CDs. I just got done with an FDIC exam and they requested shock testing 400 basis points up and nothing down. Hard to go below zero.

In terms of 5 to 7 year CDs a 15 year GNMA is probably a better way to go. Don't buy them at a premium and look at average life of 4 to 5 years. They are zero risk based as well.

Anyway nice job I could not agree with you more.

Here is a snip from my post regarding new borrow-short lend long schemes. Refer to the link at the top for a discussion of absurdly low CD rates offered by Bank of America and Citigroup, or for the full discussion about the duration mismatch problem banks are getting themselves into.

The Next Borrow-Short Lend-Long Guaranteed to Blow Scheme

Banks are setting aside billions of dollars to do something that until now was rarely heard of: making big loans to cities, states, schools and other public borrowers that otherwise might have turned to the bond market.

When Riverside, Calif., was ironing out a bond offering recently to expand its performing-arts center, several banks pitched a radical idea: Why not take out a loan instead? The city scrapped the bond plan and borrowed $25 million from City National Bank in Los Angeles.

"This was a method we'd never even heard of before," says Scott Catlett, the city's assistant finance director. He says Riverside now intends to seek a bank loan for a conference center that it had planned to build with bonds.

J.P. Morgan Chase & Co. is devoting billions of dollars to direct loans this year to both refinance deals and for new projects, according to a bank official. Last year, the bank made a few hundred million dollars of direct loans to municipalities. Now, the bank would consider making a single loan for hundreds of millions of dollars, the official said. It also is dispatching teams to explain the concept to wary public borrowers.

Citibank also is courting municipal borrowers with direct loans, according to several bond issuers. A spokesman for the Citigroup Inc. unit declined to comment.

"This used to be unheard of," says Eric Friedland, managing director of public finance at Fitch Ratings, noting that in the past, banks would occasionally loan a municipality less than $1 million to finance projects too small for a bond offering. For bigger loans, they would form a syndicate with other lenders.

It remains to be seen what land mines may be lurking for lenders and borrowers. Some municipalities are going through significant struggles, raising questions about whether they will prove good credits. And direct loans are less liquid, meaning banks can't sell them as easily as bonds.

For banks, this is a potentially lucrative business at a time when they are sitting on cash that isn't earning huge interest and are reluctant to make loans for mortgages and other areas they see as risky.

In the event of a bankruptcy, analysts say, it is unlikely that a bank extending a direct loan would be given priority over bondholders.

The city saved hundreds of thousands of dollars in issuance costs, says Mr. Catlett, the assistant finance director. Plus, he says, the interest rate is 3.85% versus at least 5% if it had floated a public offering. The term is slightly lower�21 years versus perhaps 30 years in the bond market.

"This was all new to us," he says. "I don't know now when we'll go back to the bond market. This is easier."

Fed or FDIC Should Stop this Fraudulent Scheme Now

The Fed or FDIC should step in right now. There is no way banks can secure cost of funds for 21 years for 3.85%. Moreover, the risk of default is hardly zero, and banks will not be first in line should default happen.

I think borrowing-short and lending-long is fraudulent. How can you lend something for 21 years when you only have the right to use it for 3, 5, or 7?

Want to know what those banks thinking? This is what ....

They are too big too fail

The Fed will bail them out

Cities won't default but who cares anyway because the Fed will bail them out

They have a hot pile of cash the Fed crammed down their throats at 0% and they want to put it to use

They got burnt badly on mortgages and home equity loans so they need to find something new

One idiot bank made an absurdly risky deal so like sheep they all want to do it

Right now they are all thinking there is nothing to lose from this. The Fed or Congress will bail them out at taxpayer expense if they get in trouble.

Then, when this does get out of control and blows sky high, they will all scream, "no one could possibly have seen it coming".

I's now official. Japan's demographic time bomb has gone off. However, don't look for a big crater, at least just yet, because this has started off with a whimper and not a bang.

Japan�s public pension fund, the world�s largest, said it may become a net seller of bonds to cover payments in the world�s most rapidly aging society.

The Government Pension Investment Fund, which oversees 117.6 trillion yen ($1.4 trillion), in September forecast that it would sell 4 trillion yen in assets in the business year ending March 31 to fund payouts. Sales may be less than that in the year starting April as bonds reach maturity, said Takahiro Mitani, president of the fund, known as GPIF.

�We will likely be a net seller in the market,� Mitani, a former executive director at the Bank of Japan, said in an interview in Tokyo yesterday. �We certainly have to come up with an adequate amount� to pay pensions, he said, declining to elaborate on the amount.

Sales by the fund, which helps oversee public pension funds for Japan�s 37 million retirees, come as the first of Japan�s baby boomers is set to turn 65 in 2012, making them eligible for pension payments.

The GPIF, historically one of the biggest buyers of Japanese debt, held 82.4 trillion yen in domestic bonds, or 70 percent of its assets, as of September, according to the fund�s latest quarterly financial statement. That compares with 12.6 trillion yen in Japanese stocks, or 10.7 percent, 9.6 trillion yen, or 8.2 percent, in foreign bonds and 11.5 trillion yen, or 9.7 percent, in overseas stocks, the report shows.

GPIF doesn�t plan to start investing in so-called alternative assets such as commodities, real estate, infrastructure, private equity or hedge funds because the risks don�t suit its strategy, Mitani said. �Too Early�

�It�s too early to get into alternative investments now,� Mitani said. �Japanese investors are conservative and it�s hard to justify to the public investing in asset classes such as commodities, real estate and hedge funds.�

Japan�s 10-year bond yield is the lowest in the world, data compiled by Bloomberg show. Japan�s gross domestic product shrank an annualized 1.1 percent in the three months ended Dec. 31, the Cabinet Office said on Feb. 14, and China�s economy overtook Japan�s as the world�s second largest for 2010.

People aged 65 or older will account for 29 percent of the country�s population in 2020 and almost 40 percent in 2050, according to the statistics bureau. They accounted for 23 percent population at the end of 2010, the highest among the Group of Seven countries, data compiled by Bloomberg show. That compares with 12 percent in 1990.

Japanese pension funds posted the lowest annualized growth among 12 countries between 2004 and 2009, at 2 percent in U.S. dollar terms and unchanged in yen terms, according to the survey. Brazil reported the highest growth, 24 percent in dollars, the report showed.

Thoughts and Implications

There is not going to be a huge exodus of Japanese bonds anytime soon. However, the world's largest fund has gone from being a buyer of bonds to a seller of bonds. The amount is not trivial.

82.4 trillion yen in domestic bonds is about 1 trillion in US dollars. That is a lot of pent-up supply, especially when the government is running an annual deficit of of about $240 billion with no external buyers at all.

Those factors put huge long-term upward pressures on interest rates.

Deflation Irony

The irony in this madness is that all the Japanese people want is their money back. They are not looking for appreciation. They do not have absurd pension plan assumptions like the 8% expected returns we see in the US. They do not want stocks, or real estate. They just want cash, and they want it to be worth something.

Yet, the Japanese government was hell-bent for two decades attempting to generate inflation which would have weakened the value of those bonds.

Recently, those bond holdings have been rising with a strengthening yen. However, lingering debt from preposterous deflation fighting efforts of building bridges to nowhere must be paid back.

Horns of a Dilemma

Japan choices are to default on its debt, print money to fund interest on the debt, raise taxes effectively robbing savers of their money, or undertake huge spending cuts.

The dilemma stems from years of Keynesian and Monetarist stupidity.

Japan's government pledged to balance the nation's main budget over the coming decade under its first fiscal-overhaul plan, approved Tuesday, laying the groundwork for the daunting task of tackling the country's massive debt.

Highlighting the challenge of such an undertaking, the government estimated that if growth remains modest, it may have to fill an annual budgetary gap of about 22 trillion Japanese yen (US$242 billion) by the fiscal year ending March 2021. If Tokyo were to raise that amount only by increasing the 5% consumption tax�one gauge being used�it would need to increase the tax nearly threefold.

Prime Minister Naoto Kan's government will kick off the fiscal-reform campaign by capping annual spending for the next three fiscal years and keeping new government bond issuance below 44.3 trillion yen next fiscal year. The debt amount is estimated the same as in the current fiscal year that started in April. Tokyo also promised to make "utmost efforts" to lower the amount in the following years.

The budgetary blueprints represent the first fiscal-reform plans adopted by the Democratic Party of Japan since it swept to power about nine months ago. They offer the clearest picture yet of how Mr. Kan's economic team intends to lower the nation's public-debt level, which at nearly twice Japan's yearly economic output is the worst among advanced economies.

Japanese government bonds rose as investors welcomed the plan. Lead September JGB futures finished the day up 0.34 at 140.82, while the 10-year JGB yield fell to 1.185%, its lowest level since January 2009.

But questions linger about feasibility of the framework. Absent from the blueprint are detailed spending-cut plans, such as how much to scale back individual budget categories like defense and education. There also aren't timetables for specific tax increases despite Mr. Kan's calls for doubling Japan's consumption tax in the coming years.

"The government has yet to provide details of how it can achieve the goal," said Masashi Shimominami, a bond-market analyst at Mizuho Securities. Some investors also remain skeptical over whether Mr. Kan will rally enough political support for heavier taxes on consumption, Mr. Shimominami said.

The release of the plan comes as Japanese officials shift their policy focus to fixing budgetary woes after receiving a wake-up call from Europe's deepening debt crisis. "We must make sure we avoid a situation where we lose trust in the government bond markets just like Greece and, as a result, interest rates rise sharply, putting our finances in a state of default," the guidelines said.

No Political Will For Budget Cuts

As in the US, there is no political will for budget cuts. The best the government could come up with was a plan to freeze spending for 3-years. Whoop-to-do. Bear in mind that an aging demographic will require more health care.

Will growth be sufficient to make a long-term dent in Japan's debt? I scoff at the notion. Moreover, rising energy prices will take a big bite of of Japan's trade surplus.

By the way, in case you missed it, Japan's trade surplus went negative last month. Supposedly it's a one-time thing.

Japan posts first trade deficit in almost two years

Weaker exports to key markets gave Japan its first trade deficit in 22 months, Ministry of Finance data has shown.

The trade deficit was 471.42bn yen ($5.7bn; �3.52bn) in January, with exports up 1.4%. Analysts had expected export growth to be closer to 7%.

Japan has struggled to boost exports as a stronger yen dents demand.

It recently lost its position as the world's second-largest economy to China. Changing scenario?

However, analysts said they expect exports to rebound.

That should help drive economic growth in Japan, albeit at a pace that is slower than many experts may have predicted.

One of the main reasons for the slower growth was weaker demand from China, where the government is battling inflation and signs that its economy may be overheating.

Japan is counting on increased sales to China when China is clearly overheating and will have to cut back. How do you think that fantasy is going to work out?

So, it's back to tax hikes. To do it all with tax hikes, Japan would need to hike the VAT by 200%, from 5% to 15%. Is that going to fly with the voters?

Nonetheless, let's assume Japan does hike taxes. Those tax hikes would strengthen the yen, which in turn would hurt Japan's export growth and corporate profits.

My suspicion is Japan will print money, cheapening the yen, as the most convenient way out. Printing money will make matters worse in the long haul of course, but it will put off making any tough choices now.

Allen Park, Michigan, a town of about 28,000, sent layoff notices to its entire fire department. This is a procedural move because the town is unsure how many it will need to lay off. However, the situation looks grim.

The city's finance director said today that Allen Park must lay off 25 to 30 employees by June to avoid a $600,000 deficit for the current fiscal year.

Tim McCurley said in an interview that the city sent layoff notices to everyone in the fire department to comply with a clause in the firefighters' union contract requiring a 30-day notice. He said some or all of the firefighters could lose their jobs, and that the police department faces layoffs too.

"It's not easy to lay people off," McCurley said. "No one wants to do that. It's never easy, but we are trying to work through it."

The finance director said the layoffs would only keep the city's books balanced for this year and have nothing to do with any funding cuts in Gov. Rick Snyder's proposed budget for fiscal 2012.

According to McCurley, the city faces a fiscal crunch because revenue in several areas has fallen short of projections. Collections from traffic tickets are $819,000 below what was budgeted, and ambulance billing collections are $200,000 under budget, he said.

McCurley said the city also had to refund $80,000 under order of the Michigan Tax Tribunal.

In other areas, spending has exceeded projections, including $130,000 in parks and recreation. McCurley said the city failed to budget for $150,000 for unused sick and vacation time for employees who have retired.

Overtime in the fire department is $150,000 over budget, even after firefighters agreed to limit overtime pay as part of concessions negotiated last year, McCurley said.

City Council members approved laying off the 25-person fire department Tuesday night.

Fire Chief Doug LaFond said he would be laid off as well.

But LaFond questioned the need to eliminate his entire force to make up for shrinking revenue.

"The bottom line is there aren't any other cities in the state of Michigan that are eliminating fire departments because of it," LaFond said.

The fire chief said he did not believe the entire police department was being threatened with layoff, but said the police force is about double the size of his department and could see significant cuts.

This is the second such maneuver we have seen recently where a town sent layoffs to an entire department.

I recommend Allen Park outsource its entire police and fire departments. Moreover, the Mayor should be in touch with the governor about petitioning for bankruptcy.

I have written about Detroit and Hamtramck before. Here are a few links.

It is virtually impossible to solve problems in those cities outside of bankruptcy. Contracts needs to be rewritten, pension obligations shed, and new wage structures mandated (not negotiated).

That cannot be done via collective bargaining, or indeed any kind of bargaining. The mayors and city managers of those towns should all get together and announce intention to default if the governor will not approve a valid bankruptcy process.

Libyan Rebels control most of the oil coast and have moved within 30 miles of Tripoli. Oil prices have risen along with the violence and PIMCO Co-CEO Calls Oil Spike "Stagflationary".

Thousands of mercenary and irregular forces struck back at a tightening circle of rebellions around the capital, Tripoli, on Thursday, trying to fend off an uprising against the 40-year rule of Col. Muammar el-Qaddafi, who blamed the violence on �hallucinogenic� drugs and Osama bin Laden.

The fighting on Thursday centered on Zawiya, a gateway city to the capital, just 30 miles west of Tripoli, where government opponents had briefly claimed victory. Colonel Qaddafi�s forces � a mixture of special brigades and African mercenaries � fought back, blasting a mosque that had been used as a refuge by protesters, a witness told The Associated Press.

An exiled Libyan who had been in contact with members of the opposition in Zawiya said Colonel Qaddafi�s forces attacked beginning about 5 a.m., initiating a battle that lasted 4 hours. The rebel forces fought back with hunting rifles and about 100 were killed, he said.

Fighting intensified in other cities near Tripoli � Misurata, 130 miles to the east, and Sabratha, about 50 miles west. There were also reports that Zuara, 75 miles west of the capital, had fallen to anti-government militias.

To the east, at least half of the nation�s 1,000-mile Mediterranean coast, up to the port of Ra�s Lanuf, appeared to have fallen to opposition forces, a Guardian correspondent in the area reported.

Libya�s Muammar Qaddafi, who has lost control of much of the country�s oil-rich east, appealed to citizens to end violence as his forces stepped up a crackdown on opponents and more than 100 people were reportedly shot dead.

Qaddafi blamed the uprising against his 41-year rule on �drugged kids� and al-Qaeda, speaking by telephone on state television today for the first time since a Feb. 22 speech in which he vowed to fight �until his last drop of blood.� He said he regretted the deaths during the unrest.

In the east, Qaddafi�s opponents organized committees of civilians to run and defend their cities with the help of troops who deserted his forces. In Benghazi, the country�s second- largest city, anti-Qaddafi militias in front of the courthouse were collecting weapons from people who had seized them from army supplies, a local resident said by phone, declining to be identified due to concern over reprisals.

Anti-government protesters appeared to be in control of the entire eastern coastline, Al Jazeera reported today, as clashes between pro- and anti-government forces broke out in other cities, including Sabha in the southwest, and Sabhatha and Az- Zawiyah, both west of Tripoli.

Major General Suleiman Mahmoud, commander of the Libyan army in Tobruk, told Al Jazeera that his forces have deserted Qaddafi and are siding with local residents. �We are supporting the Libyan people,� he said in a phone interview with the channel. He said Tobruk was peaceful and that residents were organizing themselves. Civil War

�The possibility of civil war only exists if Qaddafi stays,� Mohammed Ali Abdallah, deputy head of the National Front for the Salvation of Libya, the main exiled opposition group, said today.

Possibility of Civil War is 100%

I wonder what definition of "civil war" the deputy head of the National Front for the Salvation of Libya is using. That name alone implies a civil war movement, but more importantly what else can it be called with the military splits between pro and anti-government forces with rebels attacking the capital?

Clinton, El-Erian, Khelil Own Words on Libya, Oil Prices

Bloomberg has an interesting video on Libya and oil prices with Secretary of State Clinton, and PIMCO co-CEO Mohamed El-Erian.

Select El-Erian Points From Video

Western world will not grow as rapidly as before

Unemployment will be a persistent issue

Social safety nets will be stretched

On top of that we have headwinds of higher oil prices and higher geopolitical risk

Commodity prices may overshoot on stockpiling, just as happened in 2008. That is the concern of a stagflationary headwind.

If one views inflation as a function of prices there may be merit to a stagflation argument. If one properly views inflation in terms of money supply and credit, the term is confusing, because it is about prices, regardless of cause.

Please remember the origin of the term came about in the 70's when the Keynesian theory at the time was that inflation and recession could not happen at the same time. Obviously it did, proving Keynesian theory belongs in the ashcan.

This is not 1970, and the ability and willingness of consumers to expand credit at this point in time is not the same, no matter how hard Bernanke tries.

However, we are in the midst of another oil price shock, compounded by peak oil and a rapidly overheating Chinese economy. Thus the idea of "headwinds" is very real, regardless of what "flation" label one chooses to use.