Now, plenty of people, some just plain stupid, some with axes to grind write the same thing. Typically these opinions are not worth replying to, quite frankly because they are so widespread and so preposterous that one would spend all their time rebutting such nonsense. But Mr. Barsky is a special case for reasons we will address later.

In the meantime let's review some of the nonsense spewing forth from Mr. Barsky. Here goes:

In a free country, it is fair game for the media and economists to scare homeowners with words of gloom and doom, however knee-jerk, consensual and misguided they may be. The reality is this: There is no housing bubble in this country. Our strong housing market is a function of myriad factors with real economic underpinnings: low interest rates, local job growth, the emotional attachment one has for one's home, one's view of one's future earning- power, and parental contributions, all have done their part to contribute to rising home prices. Over the past quarter-century, there has been an explosion of second-home purchases, a continued influx of immigrants, and a significant reduction in existing housing inventory through tear-downs. Not all of these trends are accurately reflected in the unending stream of data published daily. Home prices on average have risen at a 6% annual pace since 1999, and 13% over the past year.

Hmmm.

It seems to me that Barsky is suggesting there is no bubble because prices are rising and there is an explosion of second home purchases. This is more or less the equivalent of saying there was no bubble in stocks in 2000 because prices were rising and people were buying more of them.

Barsky writes:

What we do have is a serious housing shortage and housing affordability crisis. Despite robust construction, unsold inventory stands at four months, well below its 25-year average. Private builders complain they can't get land permitted to meet demand. Low-income housing advocates complain housing prices are out of reach for many Americans, and that government subsidies have been slashed.

A shortage of housing? Exactly what planet is Barsky on?

Here is what I see: Millions of vacant homes:

National vacancy rates in the second quarter 2005 were 9.8 percent for rental housing and 1.8 percent for homeowner housing, the Department of Commerce=s Census Bureau announced today. The homeownership rate was 68.6 percent for the current quarter.

There were an estimated 123.7 million housing units in the United States in the second quarter 2005. Approximately 107.9 million housing units were occupied: 74.0 million by owners and 33.9 million by renters.

Given 107.9 million occupied units out of a total of 123.7 million housing units, my math suggests there are 15.8 million unoccupied units. The BLS does not break those units down into houses, condos, and apartments, but it does seem preposterous to be proclaiming a shortage. Also note that close to 70% of the people own their own home even though there are tens of thousands of unoccupied condominiums with 10 years worth of supply coming on in Florida in the next two years alone. Finally note that 70% ownership just might be the saturation rate given that many of the 30% are city dwellers that do not want to own and/or are just plain incapable of owning a house for economic or disability reasons. With all that in mind, it is well into fantasyland to suggest a shortage of houses.

Indeed, 36% of all houses sold in 2004 were for either as second homes or for "investment". Change the word "investment" to "greater fool speculation" and you have a clear picture of what is happening. People are chasing houses because they are going up. How many houses do people need anyway? I suppose if everyone needs two or three houses there might be a shortage of them.

Barsky writes:

"What we have never seen in this country is a collapse of home prices without also seeing local economic weakness or significant capacity growth. Absent those factors, housing markets just don't collapse under their own weight."

Obviously Barsky is no student of history. He ignores house prices falling for 18 consecutive years in Japan and he ignores what happened in the great depression, he ignores what happens in the oil bust in Texas, and he ignores what is happening currently in Australia and the UK. In short, Barsky takes a Pollyanna view that a recovery that has produced zero private sector jobs in spite of record low interest rates can go on booming forever.

Barsky writes:

"Herewith are some of the myths put forth by the housing bubble Chicken Littles.

• Myth #1. There is too much capacity: According to Census data, over the past 10 years, housing permits have averaged about 1.63 million units per year -- including multifamily units. Household formation has averaged 1.49 million families per year. So far, so good. But here is where the data gets murky. Roughly 6% of the new home sales were for second homes (I have seen estimates that the number is actually twice as high), according to UBS. And while there are no precise numbers on this, approximately 360,000 units every year were torn down either because they were nonfunctional, or because they were "tear-downs." When the latter two numbers are taken into account, the real number of new homes is closer to 1.2 million, or 19% fewer than the average number of new households formed each year."

Obviously Barsky has failed to take a look at BLS data showing 15.8 million unoccupied units. Barsky also seems to assume that every family needs to buy a home. Some people, especially in large cities simply do not want to buy a home. Others due to education and or income or disabilities will never be able to buy a home even if they do want one. In fact, it is this absurd ownership society that is pressuring people to buy homes (in conjunction with speculators driving up prices) that is playing a significant part of the bubble.

Barsky writes:

• Myth #2. Risky mortgage products are fueling house appreciation: Sages from Warren Buffett to Alan Greenspan have warned of the increased risk from the use of new mortgage products, particularly adjustable-rate mortgages and interest-only mortgages. The theory here is that buyers are extending themselves to make payments, and when their mortgages reset they will be in trouble. Put aside the fact that only a year ago Mr. Greenspan was advocating the use of ARMs ("American consumers might benefit if lenders provided greater mortgage product alternatives to the traditional fixed-rate mortgage," he told the Credit Union National Association last year), these concerns are wildly overstated. As virtually every mortgagee in the country knows, most ARMs are fixed rate for the first two to seven years. Virtually all have 2% interest-rate caps. The average American owns his home for seven years. Why pay several hundred basis points to lock in rates he is highly unlikely to take advantage of? Moreover, very little equity has been paid off by a homeowner in the first seven years of a 30-year loan, so consumers have been effectively overspending on interest rates for generations. As Mr. Greenspan said in his 2004 speech, "the traditional fixed-rate mortgage may be an expensive method of financing a home."

Anyone using plain common sense would realize that at zero% down, 100% financing, speculation will rise. Numerous FED officials have warned about that (and not taken it back). As for ARMs, common sense would dictate that if ARMs are used solely to buy a house that one otherwise could not afford, there is a huge interest rate risk. Indeed, those two year arms taken out two years ago near the bottom in rates are going to be a shock to lots of people that were not prepared for it. In bubbles, common sense goes out the window.

Barsky writes:

"• Myth #3. Speculators are Driving Home Prices: The media today is chock-full of stories of day-trading dot-com refugees who have found their calling buying homes and condos "on spec," with the hope of flipping the property for a higher price. Earlier this month, one Wall Street analyst published an article with the catchy headline: "Investors Gone Wild: An Analysis of Real Estate Speculation." Scary stuff. Here, again, some common-sense thinking is in order. In Manhattan, where I live, friends buy apartments kicking and screaming, convinced they top-ticked the housing market. Is Manhattan special? Are speculators flipping Palm Beach mansions? Bay Area three-bedroom homes? Newton, Mass., Tudor homes? I don't think so. Yet these markets are experiencing the same price appreciation as Las Vegas, Phoenix and Florida, where real estate investors are supposedly driving prices higher."

The reason we are seeing these stories is because they are happening. Entire buildings of condos are being sold in Florida that are now 80% investor owned. People are buying homes sight unseen. Apparently Barsky thinks that just because insanity is brewing in Manhattan as well, there is no bubble.

Finally Barsky writes:

"But bubbles happen when prices become unhinged from intrinsic value. Homes are not stocks; their 'intrinsic value' can only be in the eye of the beholder. A house has utility. Rational people might be willing to pay more for a water view, or for living close to work, or for a larger loo. Such voluntary economic decisions are neither irrational nor exuberant."

This is one of the silliest things he has said yet. Apparently Barsky believes it is impossible to have a housing bubble because there is no intrinsic value to a house. I am sorry Barsky, the fact of the matter is houses can not rise too far above wages or rent or people's ability to pay for them. That is what determines whether or not there is a bubble in housing.

Let's take a look at what some more sensible people are saying.

The Orange County Register suggests

Region's house of cards ready to topple as prices reach unsustainable levels.

"Looking at the four big counties in Southern California, over the past decade the percentage of households that can afford to buy the median- priced home (using conventional mortgage qualification standards) dropped by as much as 74 percent in Orange County (to 11 percent) and as "little" as 56 percent in San Bernardino County (to 24 percent)."

Hmmm. Only 11% of the people in Orange County and 24% in San Bernardino can afford a house. That's not a bubble?

The OC Register continues:

"But the most compelling evidence of a bursting bubble to come is the divergence of home prices and rents. In the United States over the past decade the ratio of home prices to rents has increased by almost 40 percent.

The increase is much higher in hot housing markets like Orange County (99 percent), where the ratio of median home price to average monthly rent now stands at 433:1.

To re-calibrate to more reasonable historical levels will require rents to rise sharply, which is constrained by household income growth, or home prices will have to fall, the only other possibility."

That's not a bubble?

I could site numerous statistics and numerous articles from numerous markets by people with far better credentials than Mr. Barsky but as I said, it is normally not worth the time responding to such clowns.

OK Mish just why are you bothering then?

Good question.

You see I left off a couple snips from that article Barsky wrote.

Let's take a look at them:

Mr. Barsky writes: "I am now a money manager. I currently own stocks in several homebuilders; so I am putting my money where my mouth is."

The article concludes with "Mr. Barsky is managing partner of Alson Capital Partners, LLC"

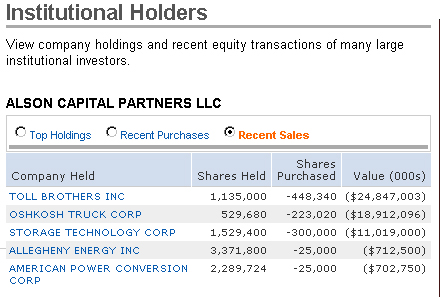

What peaked my interest in Mr. Barsky is the following chart. It is a large chart of Toll Brothers, Inc. Ownership. Click on the image and look at the second line from the bottom to see what Alson Capital Partners, LLC is doing with TOL.

That's a real eye opener isn't it?

I sense reader questions pouring in.

Yes, indeed here is a telepathically received question just now:

Mish, I see that is activity as of 03/31/2005. Is there any additional data since then?

Enquiring Mish bloggers deserve answers so let's take a look.

Hmmm. How about this?!

Let me see if I have this straight:

1) Mr. Barsky writes an article for the WSJ proclaiming there is no Housing Bubble

2) Mr. Barsky calls housing bears "Chicken Littles"

3) Mr. Barsky says "I am putting my money where my mouth is"

4) Mr. Barsky is managing partner of Alson Capital Partners, LLC

5) According to the first chart, Alson Capital Partners, LLC sold 896,680 shares of TOL in the first quarter of 2005. That was a decrease (at the time) of 28% of their original holding of 3,166,680 shares to 2,270,000 shares of TOL.

6) According to the second chart TOL reduced their shares in the second quarter by 448,340 to a total holding of 1,135,000 shares.

I am sure enquiring Mish readers are wondering what happened to the other shares since 1,135,000 + 448,340 equals 1,583,340 not 2,270,000. Unfortunately Mish has no answer to that question. At any rate that is not relevant. What is relevant is that an original holding of 3,166,680 shares has now been reduced to 1,135,000 shares. This means that Alson Capital Partners, LLC has sold 64.2% of their holding of TOL (2,031,680 shares out of 3,166,680) in the first two quarters of this year according to the charts above.

By the way, here is the source of my charts:

moneycentral.msn.com

reuters.com

Note: data may change over time which is why I captured the above charts.

Since there is a discrepancy in the numbers it not clear precisely what percentage of TOL that Alson Capital Partners, LLC has been dumping. It does seem to be huge. What is clear is the fact that two sources show Alson Capital Partners, LLC dumping TOL while a managing partner of the corporation went out of his way to defend a housing bubble in a major publication. It is also clear that Mr. Barsky failed to disclose those facts while claiming to be putting his money where his mouth is.

Given the above, I have one question for Mr. Barsky:

Is defending the housing bubble as you did consistent with Alson Capital Partners, LLC dumping huge percentages of its TOL holding?

Note: The above article originally appeared in Whiskey and Gunpowder

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

No comments:

Post a Comment