The US dollar fell sharply on Tuesday as Hank Paulson, Goldman Sachs’ chief executive, was named as the new US Treasury secretary, replacing the increasingly pressurized John Snow.Strong Dollar Policy?

Mr. Paulson has extensive links with China and some saw him as potentially better equipped than his predecessor to encourage Beijing, and the wider emerging Asian bloc, to allow a faster appreciation of the renminbi in order to help reduce global economic imbalances.

Beijing has allowed the renminbi to crawl just 1 per cent higher against the dollar since last July’s 2.1 per cent revaluation, with the currency falling to a nine-week low of Rmb8.032 on Tuesday. The importance of this issue was made clear by George W. Bush, US president, who said one of Mr. Paulson’s objectives would be to ensure the currency flexibility of the US’s trading partners.

"China has not taken kindly to pounding the pulpit and speakers who seem to convey an antagonistic approach," said Michael Woolfolk, senior currency strategist at Bank of New York. "Mr. Paulson has considerable experience in China and is well regarded over there. He could reinvigorate the discussions over currency policy."

He added: "Paulson represents a window of opportunity to accomplish a soft landing to a rapidly growing global imbalances problem. If anyone is capable of carrying this off, he is one of the best placed. The 'strong dollar' policy may quite quickly have an epitaph written for it: 'rest in peace'."

It is obvious to any thinking person that the US has had anything but a strong dollar policy. In fact a "weak dollar policy" dates all the way back to Nixon scrapping the gold standard.

More recently Treasury Secretary Snow defined a "Strong Dollar" as one that was had to counterfeit, while doing anything and everything to talk the US$ down. Since the US has been doing one thing and saying another it should be perfectly clear that the US wants a weaker dollar to help exports. Sometimes I wonder if this is nothing more than a "macho game" where strong=good and weak=bad. The US wants a strong military, strong security, and a strong economy, so of course we have to stand up for a "strong dollar" even if behind the scenes we are do everything we can to destroy it.

Unfortunately at 18-1 or 20-1 wage differentials between the US and China/India the current account deficit can not be closed by currency changes unless one proposes that the US$ will fall 90%.

The question then becomes "90% against what?" Is the RMB or YEN or anything else worth 90% more than the US$? If so why?

Weak Yen Policy?

No country that I know of wants their currency to rise at all let alone by 90% or even 50%. In fact, Japan injected $13bn into the market to prevent interest rates from rising (which would strengthen the YEN).

The Bank of Japan on Monday injected a massive Y1,500bn ($13.3bn, €10.5bn, £7.2bn) into the money market as it desperately sought to keep overnight interest rates under control.The problem for Japan is that the market seems bound and determined to force Japan into hiking. That will of course be horrid for the carry trade. I will have more commentary on the carry trade later this week. For now, let's consider whether or not the US$ is overvalued vs. the RMB.

The injection came as overnight rates once again tested the 0.1 per cent ceiling, calling into question the central bank’s ability to keep rates at “effectively zero” in line with its stated policy.

China’s Monetary Expansion

One of my favorite economists is Frank Shostak, so let's tune in to what he is saying. On May 2nd Shostak wrote an article about How China's monetary policy drives world commodity prices.

Based on the huge trade surplus with the United States, which stood at $114 bill in 2005, most analysts have concluded that the current rate of exchange of 8.017 yuan to the US dollar is far too high. However, what matters for the currency rate of exchange is the pace of money expansion relative to real economic growth — not the state of the trade account.Actions speak louder than words

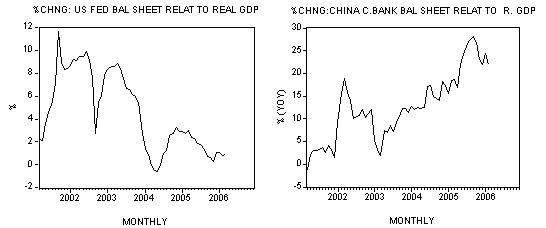

After falling to negative 1.2% in March 2001 the yearly rate of growth of the central bank balance sheet (monetary pumping) relative to real economic activity climbed to 28.2% in September 2005. In February this year the yearly rate of growth of the relative pumping stood at 22.1%.

In contrast, the yearly rate of growth of the Fed's balance sheet in relation to real economic activity fell from 11.6% in September 2001 to 0.9% in March this year.

Since China's monetary expansion relative to real economic activity has been accelerating whilst in the United States relative pumping has been decelerating, it follows that China's yuan has to depreciate against the US dollar. Yet the Chinese central bank kept the yuan unchanged against the US dollar at 8.29 from December 1996 to June 2005.

Now, the massive monetary expansion has given rise to a strong demand for capital goods (in order to expand the infrastructure). This in turn has lifted the demand for raw materials and oil. Under normal conditions if the exchange rate had been allowed to freely fluctuate the monetary pumping would have raised the price of dollars in terms of the yuan, thereby making the employment of various imported raw materials not a profitable proposition. However, once the exchange rate is kept unchanged then things become somewhat different.

The unchanged rate of exchange in fact reinforces the growing demand for raw materials. Keeping the rate of exchange unchanged whilst lowering the internal purchasing power of money through monetary pumping makes dollar-priced goods relatively less expensive for the holders of the yuan.

What allows China's central bank to sell US dollars at a subsidized rate is the massive stock of foreign reserves, which stood at US$875 billion in March this year versus US$169 billion in January 2001. If China were to appreciate its currency, as most experts advise, this, given loose money policy, will only reinforce demand for commodities from China.

The yearly rate of growth of the central bank balance sheet (monetary pumping) relative to real economic activity climbed to 28.2% in September 2005. In February this year the yearly rate of growth of the relative pumping stood at 22.1%.

Read the above then read it again until it makes sense. China has been pumping like mad, more so than the Fed. With China pumping and Japan's interest rates still hovering near zero, and with the UK's housing bubble at least as big as that in the US, is the US$ poised for the 50% drop that everyone thinks is coming? A better question is "will it drop even as much as 15% from here?"

Much of the answer to the above depends on interest rates in Japan, Europe, China, and the US, but it is by no means a certainty that the US$ is in any "short term" death spiral. Long term I think it could be in a death spiral (perhaps "IS BE" once Chinese internal demand picks up) but one can go broke trading such ideas. Just ask anyone extremely bullish on the YEN after China put in place currency bands or news that "Buffett was short the US$" hits the stands or better yet ask anyone shorting homebuilder stocks in 2004.

For now, it is clear the US housing bubble has popped and various emerging markets are blowing up. Bernanke has his test and for that matter so does China and so does Japan. No matter what anyone decides, the global liquidity game is clearly in the 9th inning. The consequences are just now starting to be felt.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

No comments:

Post a Comment