Wilson Bowden (WLB.L) said on Tuesday that fears of unemployment could further undermine the country's fragile house market, compounding a first half in which the housebuilder completed 10 percent fewer sales.

"Housing market conditions have remained subdued since the AGM (on April 27), and reservation levels have not recovered," Wilson Bowden said in a statement.

Chief Executive Ian Robertson said the market had been buoyed by news that two of the Bank of England's nine interest rate setters had voted for a cut this month. But retail weakness and high profile job layoffs like that seen at MG Rover had triggered job concerns.

"Clearly there are pleasantly encouraging noises coming out on interest rates," said Robertson. "The dilemma for me is whether these encouraging noises on interest rates will outweigh what I think is an underlying concern on the job front that hasn't been there for some years."

Economists and estate agents have warned that a rise in unemployment could lead to a sharp correction in the housing market, in contrast to the gradual slowdown seen so far.

Earlier this month, official data showed the number of people in the country out of work and claiming benefits rose for a fourth month in May, the longest stretch of increases in almost 13 years.

This is interesting because just a few weeks ago I proposed the theory that housing would not lead the decline in jobs down, but that other job losses would lead the decline in housing down.

Eventually the weight of losing manufacturing jobs, telecom jobs, banking jobs, and all sorts of other jobs and replacing them with more real estate broker jobs (all fighting to sell the same house), and "greeting" jobs at your friendly Wal-mart store is just not going to cut it.

What's happening in the UK right now is a harbinger of what is going to take place in the US with some unknown lag time. It's no secret that employment in this "recovery" is both unprecedented and amazingly weak. Yet Greenspan remains in a conundrum about long term interest rates. Is he really that stupid or is he trying to talk the economy up or both? IMO, the long bond can spot the upcoming debacle. I do not accept the theory that yields are low solely because of Chinese and Japanese intervention.

The yield curve is now as flat as a pancake. A flat yield curve is hardly conducive for tremendous profits at financial institutions. To "make up" for declining carry trades it seems banks and other lenders keep taking on riskier and riskier housing loans with lower and lower credit standards in the face of higher and higher prices. No risk is too great to keep the party going.

Indeed, BusinessWeek is reporting on this phenomenon in an article entitled "Mortgage Bankers are Desperate to Lend".

"Refinancing volume has tumbled, as has profitability, so these lenders offer increasingly sweet deals in a scramble for market share.

Why have lenders been so liberal when they run the risk that many of their marginal customers will go into default? The answer is surprising. Sure, long-term interest rates have at times continued to defy conventional wisdom and decline or hold steady even while the Fed hiked short-term rates. This gives lenders a lot of room to keep their rates to customers as low as possible.

But it turns out that's just part of the reason lenders are offering such unbelievable deals to their customers. Many lenders are just plain desperate for business, according to some experts. In a bid for market share, mortgage lenders are offering highly favorable terms to borrowers. That's forcing the rest of the industry to match their terms or lose customers.

The industry's underlying problem is simple: Overcapacity and a drop in profitability from its all-time high of 2003. And that's not the claim of an industry gadfly. It's the analysis of the sector's own top economist, Douglas Duncan, the chief economist of the Mortgage Bankers Assn. Duncan told BusinessWeek on June 23 that profits fell by 70% from 2003 to 2004 among 70 lenders that supply their internal data to the trade group."

Yes Mish readers, as silly as it might sound, we actually have an overcapacity in lending.

It now seems that all the bulls are counting on Greenspan to "save the day" with a pause in interest rates at the appropriate time. If that does not work so the theory goes, Greenspan will "save the day" by cutting interest rates. Here is a prediction for you in advance. Once Greenspan pauses the party will be over. Perhaps long over. I have another prediction for you. The next big conundrum question on the minds of economists and stock bulls will be this: "Why is the economy is not picking up with the FED cutting rates?". Here is my answer, in advance: "Just as a interest rates rising at a 'measured pace' indicated the party was still alive, falling interest rates will be a signal that the economy is falling apart faster than anyone thought it could". After all, the market rose along with interest rate hikes, is it supposed to rally when they fall too? Is everything good for stocks? Thinking about this right now, I am wondering if we get some enormous gap and crap as soon as Greenspan pauses.

Meanwhile there is little sign of significant job pickups in the US.

Let's take a look at June Layoffs in the US.

I am sure I missed some layoffs, perhaps even lots of them.

Scroll down that list. It seems staggering to me.

By the way, that was a list I complied on my Silicon Investor stock message board.

If anyone is interested in day-to-day macro economic chat feel free to join me there.

At any rate, the jobs we are adding barely keep pace with immigration and population growth. The current and likely unstoppable trend due to global wage arbitrage as well as increases in productivity is to lose high paying jobs and replace them with lesser paying service jobs. Real wage growth is negative, and that unfortunately includes pay raises for CEOs, bankers, brokers and other fat cats at the upper ends of the scale that are doing phenomenally well. On balance, I suggest wage data is far worse than it looks. Supporting evidence for this theory is increasing debt and consumer spending furnished by cash out refis.

Bear in mind we have not yet felt the mammoth layoffs announced earlier this year in banking and telecom mergers. Nor have we felt the affects of upcoming GM layoffs. Tens of thousands of announced job cuts will start filtering thru in the second half of the year.

Of course the cheerleaders on CNBC and elsewhere keep touting unemployment without mentioning the participation rate, wage growth or anything else that I talked about in the following blogs:

Where the hell are the jobs?

Searching For Jobs

Making Sense of April Payroll Numbers

Outsourcing the Soul of the US

Real Inflation Adjusted Wage Growth

Very few mainstream economists are taking a good hard critical look at the job situation. Paul Kasriel and Asha Bangalore, both from the Northern Trust in Chicago are two of the best hard-hitting exceptions.

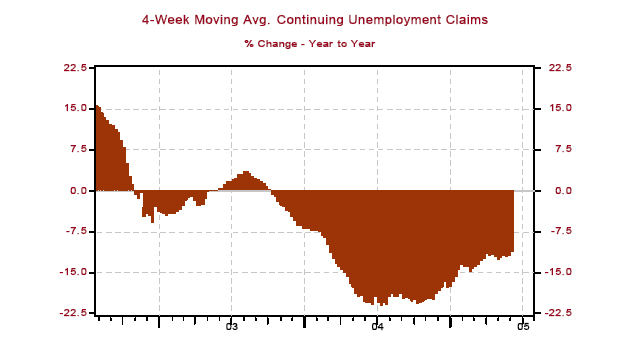

Consider the following charts by Paul Kasriel from an excellent Northern Trust article entitled Labor Market Continues To Show Less Vigor.

Initial Unemployment Claims

Continuing Unemployment claims

Instead of looking at seasonally adjusted data on top of ridiculous birth/death assumptions, on top of falling participation rates in a "recovery", on top of people running out of benefits so they are no longer considered unemployed, on top of whatever political bias someone may have to distort the adjusted numbers, those charts are where the rubber meets the road. Neither chart is very pretty, unless you are a housing or stock market bear. Take a good hard look at the trends.

Greenspan and Snow and cheerleading economists everywhere want you to believe that a flat yield curve "is different this time" and that although we created no jobs to speak of with interest rates at 1% (note that private sector job growth under Bush is still net negative or perhaps just recently slightly positive), that somehow job growth is just around the corner. Get real.

If 1% rates could not produce jobs what can? Of the jobs that we did create, Asha Bangalore had this to say: "Employment in housing and related industries accounted for about 43.0% of the increase in private sector payrolls since the economic recovery began in November 2001."

Wow. What happens to those jobs when housing turns down? Most economists want you to believe the housing party can last forever. Well I have news for them. The party is almost over.

If you want to see a strong correlation between consumer spending and home prices look no further than UK Headed for Recession.

Inflationists believe that consumers will keep spending with the job losses and wages losses in the upcoming housing debacle. I don't buy it and consumers in the UK don't seem to buy it either.

Regardless of what any of the cheerleaders want you to believe, the tightening of the yield curve is not good for profits or hiring or anything else for that matter. The anemic job growth we are seeing now is eventually going to spill over into the last strong sector we have left: housing.

The question is not whether or not the US will follow the UK. The pertinent question is: "exactly how big is the time lag?" I think the lag will be about 6 months to a year. But judging from housing and job action in the UK and Australia, we are probably 4-6 months in already. In other words, I look for things to get worse, a lot worse, sometime within the next 6 months or so. Perhaps it has already started.

Once wage and job losses start affecting housing sales, our economy will fly apart like a Hostess crumb-cake tossed into a dishwasher. This will start a mammoth Japanese style liquidity trap from which Greenspan and the FED will have no escape.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

No comments:

Post a Comment